Every year, Capgemini publishes a Financial Services Analysis that I read with great interest. This year, they’ve added a World FinTech Report, and between the lines, these reports reveal a lot of fascinating insights. FinTech is definitely on the rise, but banks still have a competitive edge that they can use to stay in the lead. However, they should be cautious. A new generation is coming of age, and the customers of the future appear to be less loyal to traditional banks. That means the current big players could lose their existing advantage.

Is FinTech storming the market place?

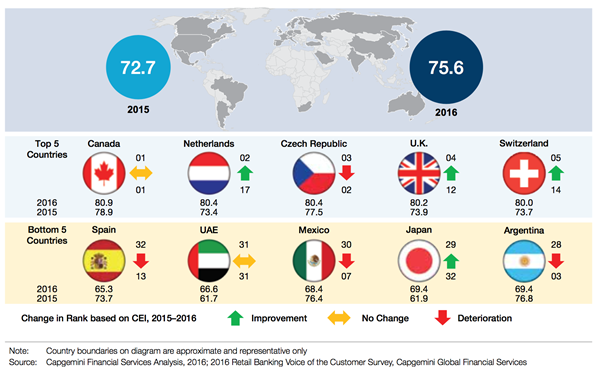

If you ask people, the general impression seems to be that FinTech is storming the market place. And in a way it is. However, in countries like Canada, and large parts of Western Europe, consumers trust their traditional banks more than they trust FinTech companies. The reports show the Customer Experience Index which indicates whether people in a country are pleased with the services of their banks or not. With a score of 80.4, the Netherlands occupies the second place in the CEI Index, just after Canada, while Germany ranks twelfth with a score of 77.1.

The Netherlands used to occupy the 17th position, and has therefore risen quite dramatically in its appreciation of the banking channel. That is remarkable, considering that offices have been closing down in rapid succession over the last years. Customers now visit their bank mostly for specialized services. But since these are the services that are valued highly by customers, the overall satisfaction with the banking channel has gone up.

It’s easy to see the deeper reasons for this success. Banks have already established a relationship with their clients, the information about them is stored in their databases, and they can access that through their back-office. This makes their base of operations much stronger than that of FinTech companies.

FinTech as blessing in disguise

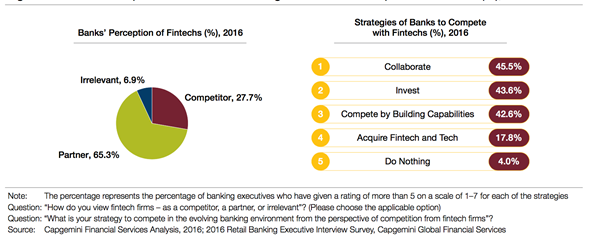

On the other hand, traditional banks don’t position themselves as clearly as FinTech companies, and they often have trouble being as innovative as their FinTech competitors. This threatens their position. But in this respect, FinTech can also be a blessing in disguise, and one that big European banks should welcome. In order to catch up with FinTech companies, traditional banks have a few options. They can either try to emulate the strengths of FinTech companies on their own – which would take an incredible amount of time and effort – or they could focus their efforts on what FinTech companies deliver and then decide on how to cooperate with them, or ultimately to acquire them or their innovative solutions.

Banks have already established a relationship with their clients.

This makes their base of operations much stronger than that of FinTech companies.

Opportunities in different areas

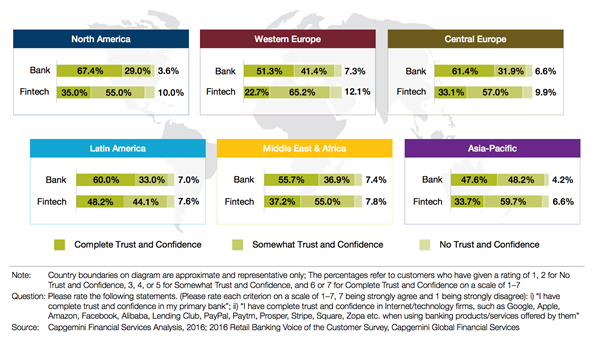

The high score of the Netherlands in the CEI Index indicates that while customers may have lost much of their trust in the banking sector as a whole, they do have great trust in their own bank and their own financial advisor. Bankers themselves attribute that trust to the longstanding relationship they have with their customers, and to their robust risk management. They feel that FinTech companies have opportunities when it comes to cards & payments, granting loans and stimulating financial awareness. Services like investment, financial advice and mortgages are too complex for consumers to leave to FinTech companies, according to bankers. They expect customers to look to banks for solutions in these areas. Of course FinTech companies deliver services in these areas, but until now they are quite basic ones. Today, when a client faces a more challenging situation, he feels a need to verify his choice with an advisor. In the future, FinTech can and will take over more of this market.

Banks and FinTech will cooperate more closely

Two things matter in the market: trust and offering new functionalities. My belief is that banks will aim to cover the more interesting aspects themselves, and will seek partnerships with FinTech companies for the remaining services. This might leave a group of FinTech companies, capable of binding customers by providing special kinds of services. By cooperating with FinTech companies in other areas, banks will try to maintain high-quality propositions, and they will probably be successful in that endeavor.

It’s unlikely that FinTech will signal the end of traditional banking. The Netherlands has one of the highest internet connectivity scores in the world, and ranks equally high in its use of mobile devices. In our use of FinTech companies, however, our position doesn’t come higher than 30. The simple explanation is that only 22% of the Dutch trust FinTech over traditional banks. And this makes sense, for why would you do business with FinTech companies if you are perfectly satisfied with the relation with your bank?

New brands are facing an upward struggle: people are less inclined to trust them with large sums of their hard-earned savings, simply by pushing a button.

Gen Z may change the game

Still, the trust needed to engage with robo advice platforms is growing. While 50.2% of customers already do business with at least one FinTech provider globally, the tech-savvy among them are twice as likely to use FinTech companies to supplement traditional services (67.3% versus 33.6%). And unsurprisingly, these customers are mostly found among the younger population, known as Gen Z. As Gen Z and tech-savvy customers become more prominent over time, the percentage of customers that turn to non-traditional firms for traditional services will inevitably grow. This creates a solid foundation on which FinTech companies can build trust. Their current customers already value FinTech companies higher when it comes to offering value for money, and timely, efficient service.

Traditional banks have left a gap of unmet customer needs that FinTech companies can and will exploit.

Banks can do better if they let new initiatives work for them

A whopping 82% of FinTech customers choose these providers because they offer ease of use. They’re faster, cheaper and include features that banks do not offer.Traditional banks have left a gap of unmet customer needs that FinTech companies can and will exploit. The efforts of banks to foster innovation have fallen short, compared to the effort they have put into them.

By opening themselves up to new initiatives, banks can offer their customers much more, and diminish the chances of ever losing them.

The ever rising number of FinTech firms doesn’t necessarily mean that they will raise a lot of volume in D2C business. After all, how are customers supposed to choose between all these offerings? The future of innovative Fintech lies in bringing interesting functionality to the established B2B or B2B2C business that they can connect with. The innovation will lie in going from Robo 1.0 (execution only) to Robo 2.0 (guidance and/or advice) and finally to Robo 3.0, which is financial planning for the mass-market. A hybrid model will most likely prevail there, allowing clients to fall back on the help or advice of a person.

Contact

Iwan Schafthuizen

Managing Director Business Development and PlatformsRelated Insights

-

09 April 2024PRESS RELEASE: Ortec Finance releases integrated economic and climate scenarios

09 April 2024PRESS RELEASE: Ortec Finance releases integrated economic and climate scenariosFind out more about the industry’s first integrated economic and climate risk management tool.

-

03 April 2024PRESS RELEASE: Ortec Finance selected once again as a leading WealthTech provider within top ranking list

03 April 2024PRESS RELEASE: Ortec Finance selected once again as a leading WealthTech provider within top ranking listThe prestigious WealthTech100 2024 list, distinguishes the most innovative technology providers that are transforming the operations of investment firms, private banks, and financial advisors. Ortec Finance selected once again!

-

02 April 2024PRESS RELEASE: Ortec Finance and Salesforce Partner to Deliver AI and Data-Driven Personalized Finance and Goal Planning for Clients

02 April 2024PRESS RELEASE: Ortec Finance and Salesforce Partner to Deliver AI and Data-Driven Personalized Finance and Goal Planning for ClientsOrtec Finance and Salesforce, the global leader in CRM, announced a partnership to deliver a more data-driven personalized finance and scalable wealth advice experience for Ortec Finance customers using Salesforce Financial Services Cloud (FSC).

-

19 March 2024In-House Student Day: Thursday 30 May, 2024 - Rotterdam

19 March 2024In-House Student Day: Thursday 30 May, 2024 - RotterdamCalling all students! Join us for an unforgettable day of insights and inspiration at our exclusive In-House Student Day.

-

12 March 2024WEBINAR: 2024 Ortec Finance Climate Scenarios

12 March 2024WEBINAR: 2024 Ortec Finance Climate ScenariosLearn how to utilize Ortec Finance’s 2024 climate scenarios to help inform investment decisions

-

29 February 2024Client Conference 2024 program is released

29 February 2024Client Conference 2024 program is releasedMay 15 & 16, 2024 Ortec Finance’s clients gather in Amsterdam for an in-person Client Conference. The event takes place in the iconic Eye Film Museum.

-

26 February 2024The Key to Conversations on Risk: Discussing Financial Goals

26 February 2024The Key to Conversations on Risk: Discussing Financial GoalsRisk is often seen as complex and intimidating when it comes to investing. Yet, discussing financial goals is a highly accessible entry point for clients to engage with risk.

-

23 February 2024Ortec Finance's 2023 customer satisfaction survey shows high scores

23 February 2024Ortec Finance's 2023 customer satisfaction survey shows high scoresThis consistent positive feedback reflects the strong rapport we share with our clients around how our solutions solve their challenges.

-

12 February 2024PRESS RELEASE: Ortec Finance appoints Hens Steehouwer as Chief Innovation Officer

12 February 2024PRESS RELEASE: Ortec Finance appoints Hens Steehouwer as Chief Innovation OfficerHens will responsible for integrating climate risk and expanding AI capabilities