Ortec Finance, a leading provider of top-down climate scenario analysis for financial institutions, today released its updated 2026 climate scenarios, which for the first time include the impact of physical climate risk on sovereign debt holdings.

In Ortec Finance’s latest higher warming scenarios, which are closest to the current trajectory of global warming, physical risk caused by extreme weather events and climate tipping points lead to sharp and lasting declines in GDP. This would also result in much reduced tax revenues and large uninsured losses.

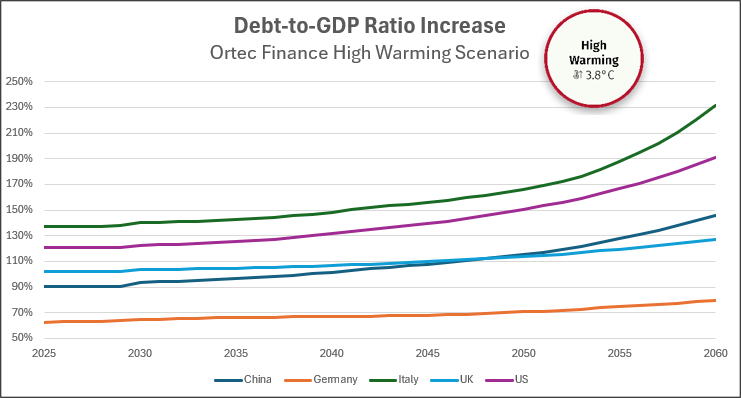

The latest figures show that the costs of climate change alone could drive up debt-to-GDP ratios in the UK to 114% by 2050 from 102% in 2025, and to 151% from 121% in the US.

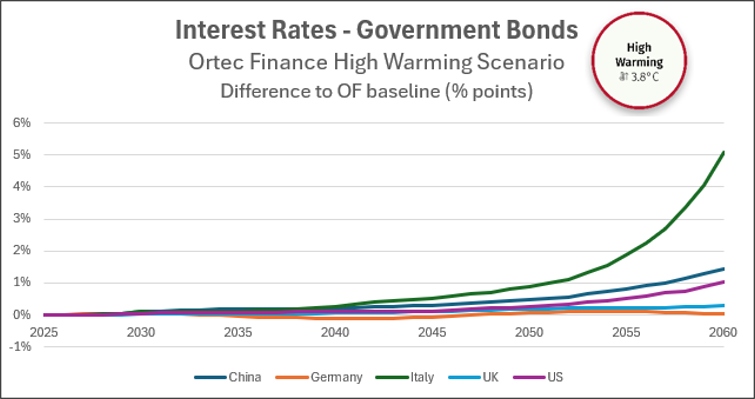

“In our view, the adverse impact of climate change on global GDP, levels of insurability and ultimately the ability of governments to plug the funding gap through sovereign debt markets has been an important missing link in the total portfolio assessment of climate risk,” said Maurits van Joolingen, Managing Director for Climate Scenarios & Sustainability at Ortec Finance. “While climate risk is a systemic issue, it doesn’t affect all regions equally, necessitating a regional approach to investment strategies and sovereign debt portfolios, especially given their long maturities. It’s important for pension funds to evaluate how physical and transition climate risks influence national GDP, debt-to-GDP ratios, insurability and ultimately interest rates.”

Pension funds allocating to private assets need to understand climate impact now

As pension funds search for higher returns and governments exert pressure on fund managers to invest locally, many fund managers are increasing their investments in private assets.

“Pension funds investing in private assets need to be aware of the physical climate-related risks associated with holding these assets, which are typically less liquid and held for much longer than equites or bonds. Investments made now into infrastructure or real estate typically have a 15-year plus time horizon, so these are highly likely to be affected by rising physical climate risks,” added van Joolingen.

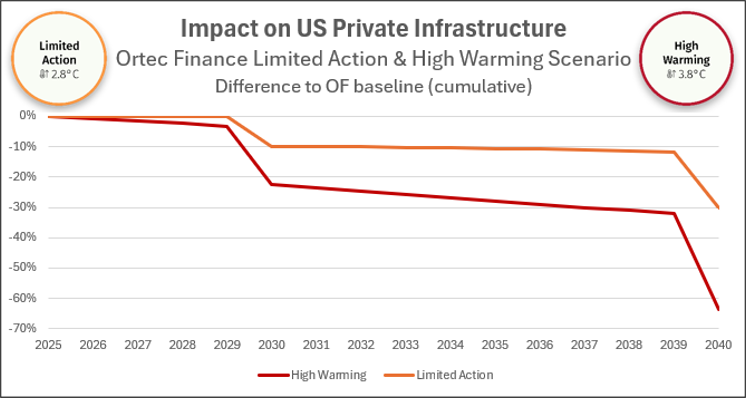

Over a 15-year time horizon, private infrastructure assets in the US will suffer a 30% loss in returns, in comparison to their baseline expectations*, under a Limited Action scenario, where temperatures increase by 2.8 °C by 2100.

Losses will exceed 60% in a High Warming scenario, where temperatures increase 3.8 °C by 2100. In Europe, losses range from 15% in a Limited Action scenario to over 30% in a High Warming scenario.

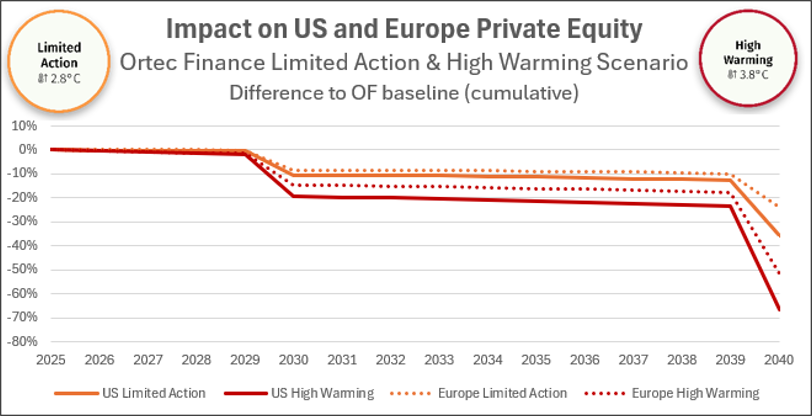

Over the same time period, US private equity underperforms by over 35% in a Limited Action scenario and over 65% in a High Warming scenario, while in Europe private equity underperforms by over 20% in a Limited Action scenario and over 50% in a High Warming scenario.

Losses under these scenarios occur as longer-term physical risks begin to be priced into financial markets.

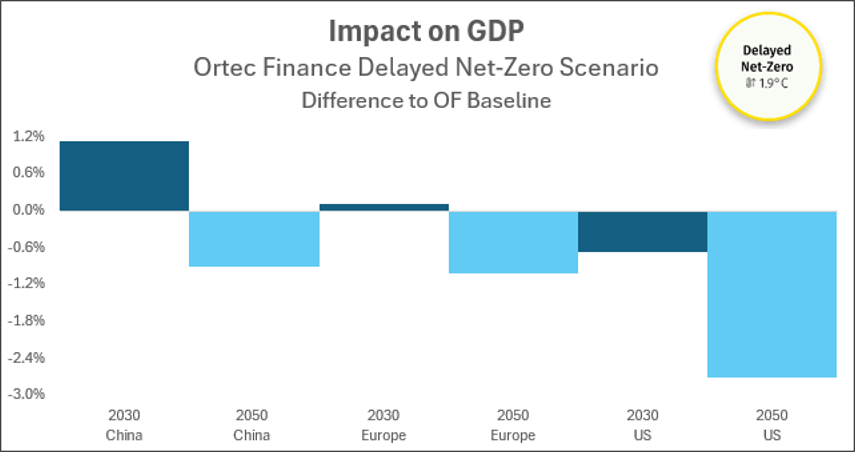

Delayed transition to net zero signals financial market disruption and sustained macroeconomic strain.

Ortec Finance’s analysis continues to indicate that achieving net zero by 2050 is no longer feasible, as highlighted in its 2025 update, pointing investors to focus towards its Delayed Net-Zero scenario.

“The lack of progress in implementing transition policy, compounded by the current geopolitical volatility and weak commitment from major governments, suggests that investors must understand how sudden financial market disruption and sustained macroeconomic strain from 2°C warming could materialize under a delayed transition,” added van Joolingen.

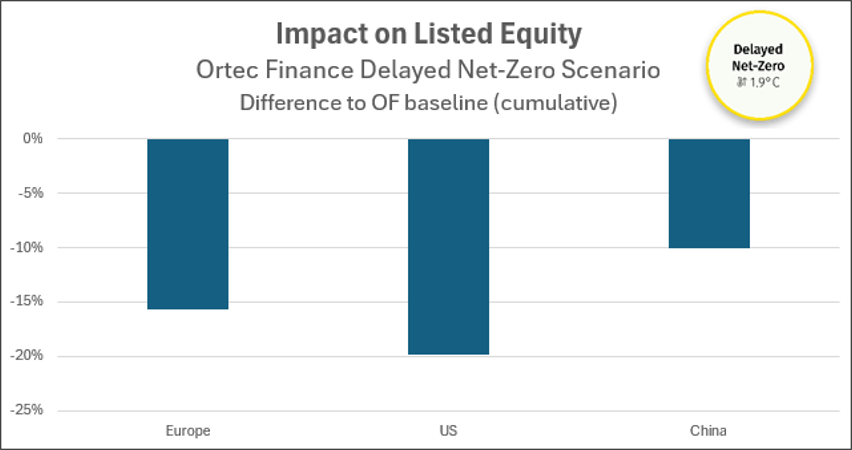

Under Ortec Finance’s Delayed Net-Zero scenario, returns on European listed equities could decline by over 15% and US listed equities around 20% by 2030.

Commenting on the latest scenarios, Sophie Heald, Senior Climate Specialist at Ortec Finance, added: “The results of our 2026 scenarios highlight the widespread impact posed by rising physical climate risks, and how this systemic impact influences insurability, a growing concern amongst investors. With physical risks remaining insufficiently priced in across all asset classes, investors who understand these climate-induced risks have the ability to access first mover advantage, with a realistic and comprehensive climate risk assessment derived from plausible robust scenarios.”

* The Ortec Finance Climate Scenarios are created as deviations from a baseline scenario (OF baseline) that reflects public reference climate scenarios in the 2°C to 3°C global warming range.

Climate Scenarios & Sustainability 2026 Ortec Finance Climate Scenarios

Contact