Inflation has put the profitability of both Life and Non-Life insurers under strain. In light of the risk of sustained raised inflation, the Prudential Regulatory Authority (PRA) has urged insurers to factor in these effects and to determine their long-term impact. Given that inflation has the potential to impact businesses in different ways, this exercise is far from trivial.

How inflation affects insurance

The effects of inflation can be felt by insurers through a variety of channels that impact certain lines of business differently. For example, Life insurers might face a drop in sales or experience a higher termination rate, either via higher lapses or by increased non-renewal. This kind of ‘demand destruction’ typically starts slowly, but gains momentum once inflation persists.

To Non-Life insurers the inflationary pressure is felt mostly in rising claim costs, being a ‘cost-driven’ phenomenon and the result of higher input prices for basic materials and labor. Especially for insurers that provide in-kind policies, this ‘claim inflation’ appears to have moved even faster than general CPI, causing additional concern.

Not surprising, therefore, is the announcement made by PRA to focus more on inflation’s long-term impact. As a prelude to this, the UK regulator has urged insurers to factor in all inflation effects and to come up with ways to manage them.

Managing inflation pressures

Depending on their business type/mix, insurers have limited options to alleviate inflation pressures, each with their own pros and cons. These include:

- Adjusting asset allocations

Typically, well designed insurance portfolios tend to hold up relatively well under inflation scenarios. However, insurers could consider alternative investment strategies with increased exposure to real assets, or other investments that offer higher inflation protection. Nevertheless, the drawbacks of this strategy can be higher volatility or a larger mismatch in terms of duration and liability cash flows.

- Capping inflation risk in new products sold

Many Life products are still sold without upside restrictions. Especially for longer dated contracts, like indexed annuities or universal whole life, the cumulative effect of inflation compensation could be high. Considering that these risks cannot always be fully priced in, insurers might wish to avoid these risks completely, for example by introducing an indexation cap in new product terms.

- Differentiating premiums to claim conditions

For Non-Life insurers the price renewal cycle is relatively short. This allows for much more flexibility in considering alternative pricing strategies. Insurers might want to base their pricing on different levels of inflation, e.g., including distinguishing between general price increases versus core CPI. As products tied to the latter proved to be less susceptible to inflation volatility, these could be offered at a more attractive rate.

Managing the additional complexity

To determine the impact of inflation and to evaluate the possibilities of mitigating them, insurers need to consider the overall impact on their businesses, derived from a consistent risk modelling framework. What can make the evaluation particularly challenging, is the number of elements impacted by inflation: pricing, capital requirements, profitability and commercial aspects, are inter-linked but often at different cadences, requiring a holistic approach.

Scenario analysis forms a powerful approach to support decision making in uncertain environments. Both deterministic as well as stochastic methods can combine inflation scenarios with strategic decision making as a way to analyze the overall impact. As an example, it is possible to demonstrate the result of stochastic simulation for an insurer offering indexed annuities. The results are based on two different economic environments, i.e. a baseline and stagflation. All other factors are fixed.

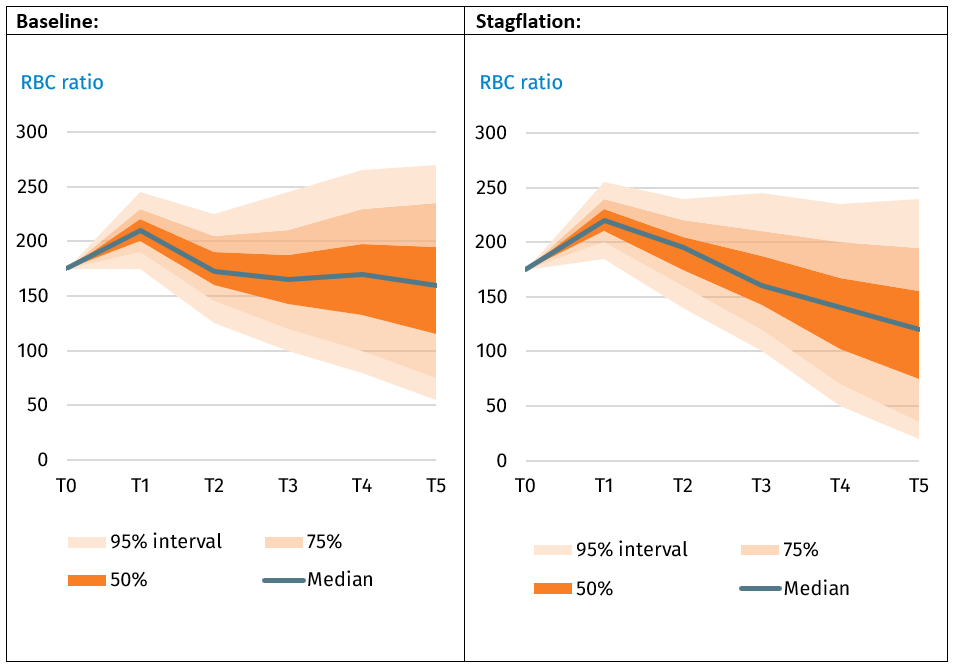

Example 1: No inflation cap

To assess the overall impact of inflation, analysis could start from investigating the Life insurer’s capital ratio, here based on the RBC framework. By keeping all else fixed, but considering only a different economic environment, the above results suggest that a period of stagflation would be significantly harmful to capital.

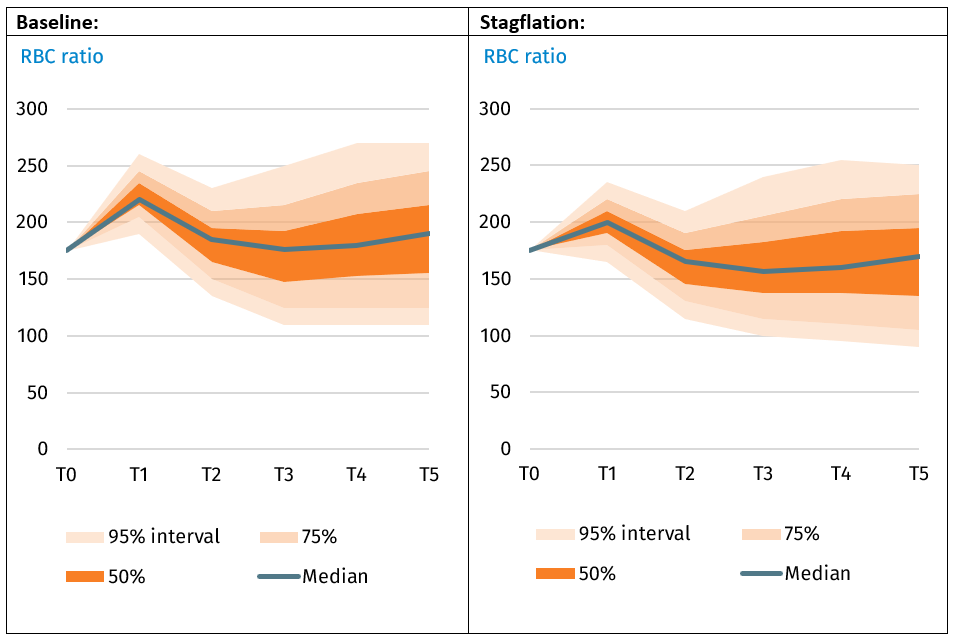

Assume now that as a mitigating option, this insurer will put a capping system in place, limiting the indexation to a long run historical average, one could compare the impact on a like-for like basis.

It appears that by enabling the capping system, this insurer has – on an average basis - improved its ratio development, both in terms of its expected mean and in terms of volatility. The relative benefits are stronger under stagflation, where the capping system pays off more.

Off course mitigating options like this cannot be assessed in isolation. In fact, by changing the indexation terms there could be less demand for this product. By combining all relevant factors stepwise, investors can find out their true sensitivity to inflation and formulate an optimal strategic response.

The previous examples were produced by using Ortec Finance’s ALM platform GLASS. For more information, please visit our ALM for insurance companies page.

Contact

Sander Dekker

Senior ConsultantRelated Insights

-

03 August 2026Quarterly Outlook: Q3 2026

03 August 2026Quarterly Outlook: Q3 2026The outlook is based on the Ortec Finance Economic Scenario Generator (ESG) and offers our perspective on recent developments in the economy and capital markets.

-

28 July 2026Webinar: Funding ratio attribution for asset owners under higher interest rates

28 July 2026Webinar: Funding ratio attribution for asset owners under higher interest ratesLearn how to develop a funding/solvency attribution framework that encompasses a comprehensive view of the fund’s performance.

-

28 July 2026Ortec Finance selected by Ostrum Asset Management for its GLASS ALM and PRISM Machine-Learning Optimization tools

28 July 2026Ortec Finance selected by Ostrum Asset Management for its GLASS ALM and PRISM Machine-Learning Optimization toolsOrtec Finance, a leading provider of investment modelling solutions, today announced that Ostrum Asset Management, an expert Insurance and Institutional investment manager and affiliate of Natixis Investment Managers, has selected Ortec Finance’s GLASS ALM and PRISM Machine-Learning Optimization solutions to provide an enhanced investment solutions offering to its insurance and pension clients.

-

27 July 2026Top-down or bottom-up? How should institutional investors manage climate risk?

27 July 2026Top-down or bottom-up? How should institutional investors manage climate risk?Evaluate the top-down and bottom-up approaches to managing climate risk and examine which is more effective at improving portfolio resilience

-

22 July 2026Article GLASS PRISM: The Evolution of Insurance Asset Portfolio Optimization

22 July 2026Article GLASS PRISM: The Evolution of Insurance Asset Portfolio OptimizationFollowing the launch of GLASS PRISM, Ortec Finance attracted significant media attention, with industry publications exploring how the solution is transforming portfolio optimization for institutional investors.

-

20 July 2026Articles GLASS PRISM: A New Standard in Strategic Asset Allocation

20 July 2026Articles GLASS PRISM: A New Standard in Strategic Asset AllocationThe GLASS PRISM launch introduces targeted SAA powered by scenario-based machine learning. Discover what's driving industry attention.

-

18 June 2026Virtual panel discussion #2 (Asia-Pacific): Extending the lens on climate change to capital market assumptions

18 June 2026Virtual panel discussion #2 (Asia-Pacific): Extending the lens on climate change to capital market assumptionsHear thought-provoking perspectives on climate change’s impact on capital market assumptions, including short and longer-term market pricing dynamics

-

18 June 2026TPA Quick Wins Article

18 June 2026TPA Quick Wins ArticleHow to adopt the TPA framework without fully transitioning to TPA.

-

05 June 2026Strategic Asset Allocation in the “TW-ICS” Era

05 June 2026Strategic Asset Allocation in the “TW-ICS” EraHow Taiwanese insurers can modernize strategic asset allocation and strengthen long-term resilience.