Climate scenario analysis designed for investment decision-making

Identify and understand how physical climate risks, low-carbon transition impacts and associated market pricing responses could systemically affect investment portfolios, financial markets and economies.

ClimateMAPS is Ortec Finance’s top down climate scenario analysis solution, developed in partnership with Cambridge Econometrics, that enables financial institutions to quantify climate change risks and identify opportunities, across all asset classes, macroeconomic variables and sectors.

Prepare for climate change. Translate plausible climate futures into quantified financial impacts.

Measure, monitor and manage multi-asset portfolio climate risk and opportunities

Manage portfolio-wide climate risks with our in-house Ortec Finance Climate Scenarios, that:

![]()

Comprehensive

By translating climate risk and opportunities into all asset classes, macroeconomic variables, conventional and green benchmarks and regions and sectors

![]()

Realistic

By delivering a real-world assessment of systemic transition, physical and market pricing risks

![]()

Integrated

By utilizing a range of advanced models to deliver results that can be integrated with traditional risk analysis and asset liability management (ALM) platforms

Improving portfolio resilience with Ortec Finance Climate Scenarios

Our proprietary climate scenarios, first developed in 2018 and updated annually enable investors to:

- Obtain a realistic transition risk assessment that captures broader real-economy impacts - including differences in risks and opportunities across regions and sectors.

- Evaluate physical risks including tipping points and non-linear escalating impacts, aligned with the IFOA’s recommended use of a logistic damage function

- Gain a comprehensive climate risk view for multi-asset institutional portfolios covering detailed asset classes, benchmark and sector holdings

- Capture impacts from insufficient pricing-in across the investment horizon - emerging gradually, through shocks, or sentiment shifts

- Examine and compare deeper narratives, including methodology, scenario drivers, climate science as well as policy and regulatory developments.

This supports pension funds and insurers to undertake stress-testing, strategic asset allocations, investment strategy development and stakeholder engagement in addition to reporting, ISSB-aligned disclosures and peer benchmarking.

Using the same modeling framework, climate scenarios can also be customized to a financial institution’s views and assumptions as a bespoke climate scenario.

For reporting, disclosures and peer benchmarking purposes only, ClimateMAPS is also available with NGFS Phase V climate scenarios.

Learn more about the differences and how to choose the right scenarios to meet your investment objectives.

Utilizing Ortec Finance Climate Scenarios

Deliverables |

Application |

|

AnalyticsEconomic variables for 20+ countries/regions 700+ financial variables across all asset classes, including green benchmarks |

AnalysisUnderstand the financial impacts and outcomes under a wide range of plausible climate change futures |

|

Insights30+ sector-specific impacts for equities and credit Geographical insights including heatmaps |

Stress-testPerform a portfolio climate stress testing exercise, including an assessment of sovereign default and credit risk in fixed income portfolios.

|

|

AssessmentComprehensive total portfolio analysis including dataset and detailed supplementary report |

Strategy designIntegrate climate change into investment beliefs, capital and strategic asset allocation as well as selection and monitoring |

|

BreakdownIn-depth breakdown of transition, physical and market pricing climate risks for all macroeconomic and asset class impacts |

Risk managementAssess and mitigate climate change from a financial risk management perspective |

|

DashboardInteractive web-based tool featuring dynamic charts, maps and videos and explanations for comparison, with ongoing support and training |

ReportingUndertake stakeholder engagement and climate-related reporting and disclosures, meeting ISSB’s requirements to include at least two scenarios to evaluate resilience – one pursuing 1.5°C and one exceeding 2.5°C by 2100 |

Translating the cost of climate change for pension funds and insurance companies worldwide

Our Climate Scenarios & Sustainability team undertake an annual analysis to assess how climate risk is affecting pension funds and insurance companies globally, using the latest release of our Ortec Finance Climate Scenarios

Climate scenario analysis for financial institutions

ClimateMAPS can meet the climate risk management needs of diverse financial institutions.

Learn more about how our climate scenario analysis solution can help pension funds assess the implications of climate change for long-term portfolio resilience and the financial stability of pension beneficiaries, while enabling insurance companies to evaluate climate change’s impact on short-term liabilities, investment targets, and overall balance sheet resilience.

Understand total portfolio exposure across traditional investment and climate risks

Using ClimateMAPS to identify the impacts on asset class returns of optimized portfolios generated based on ALM studies against the same baseline determined in GLASS.

Support private asset investment decisions

Combine regional, sectoral, macroeconomic, and asset-class impacts to identify private asset opportunities and actively drive investment in the low-carbon transition from a total portfolio perspective.

![]()

Our climate risk management insights

Webinars

Evaluating the pricing impacts of

climate risks

Watch our webinar to explore how our climate change affects asset performance and valuations.

2026 Ortec Finance Climate Scenarios

Watch our webinar to learn about the latest Ortec Finance Climate Scenarios - focusing on the relative likelihood and how the scenarios closest to the current climate trajectory could impact sovereign debt, private assets and insurability.

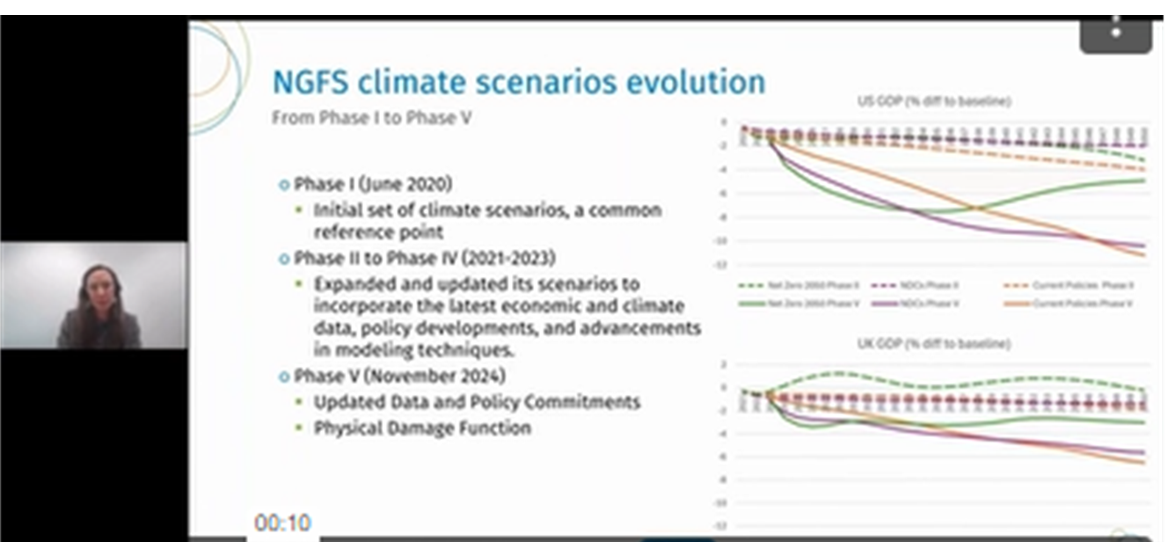

Utilizing NGFS climate scenarios for climate risk analysis

Watch our webinar to understand how NGFS climate scenarios can be utilized for assessing the financial impact of climate change.

Want to learn more about how ClimateMAPS can help financial institutions prepare investment portfolios for the impacts of climate change?

Receive the latest sustainable finance and climate risk management insights

Previous topics include how a climate change-driven insurability crisis could compromise global financial stability and whether climate change should influence investment strategies and capital market assumptions (CMAs).

Subscribe to Radar

Contact

Maurits van Joolingen

Managing Director, Climate Scenarios & Sustainability

Hamish Bailey

Managing Director UK, Head of Insurance & Investment

Richard Boyce

Managing Director, North America

Stefano SJ Lee

Managing Director - Asia Pacific

Stacy Howlin

Managing Director, United StatesRelated Insights

-

06 May 2026Webinar recording: 2026 Ortec Finance Climate Scenarios

06 May 2026Webinar recording: 2026 Ortec Finance Climate ScenariosLearn about the 2026 release of our proprietary climate scenarios, designed to help manage portfolio risk exposure and resilience to climate change

-

29 April 2026Extending the lens on climate change: Beyond investment strategies to investment policy and capital market assumptions

29 April 2026Extending the lens on climate change: Beyond investment strategies to investment policy and capital market assumptionsWe explore the global investment community’s views on how climate change is shaping investment decision-making and risk management frameworks.

-

21 April 2026Ortec Finance warns of insurability and sovereign debt crisis with latest climate scenario update

21 April 2026Ortec Finance warns of insurability and sovereign debt crisis with latest climate scenario updateLearn why insurers should understand how an insurability crisis could be triggered and threaten overall global financial stability

-

21 April 2026Ortec Finance warns pension funds on impact of climate risk to sovereign debt and private assets in its 2026 climate scenario update

21 April 2026Ortec Finance warns pension funds on impact of climate risk to sovereign debt and private assets in its 2026 climate scenario updateLearn why pension funds should understand the financial and economic impact of physical climate risks to sovereign debt and private assets

-

03 March 2026Ortec Finance Wins Insurance Asset Risk Technology Provider of the Year

03 March 2026Ortec Finance Wins Insurance Asset Risk Technology Provider of the YearOrtec Finance is proud to announce that it has been named Insurance Asset Risk Technology Provider of the Year at the Insurance Asset Risk Awards 2026. The award recognizes leadership in delivering advanced, transparent and practical technology to help insurers and asset managers make better investment and risk decisions in an increasingly complex world.

-

26 February 2026Virtual panel discussion: Extending the lens on climate change: Beyond investment strategies to investment policy and capital market assumptions

26 February 2026Virtual panel discussion: Extending the lens on climate change: Beyond investment strategies to investment policy and capital market assumptionsHear thought-provoking perspectives on climate change’s impact on capital market assumptions, including short and longer-term market pricing dynamics

-

18 February 2026Breaking down the Bank of England Prudential Regulation Authority’s guidance on the management of climate-related risks for UK insurers

18 February 2026Breaking down the Bank of England Prudential Regulation Authority’s guidance on the management of climate-related risks for UK insurersExplore the BoE’s expectations on how UK insurers should manage climate risks across their balance sheets and embed them into risk management frameworks

-

26 January 2026Forward Analytics partners with Ortec Finance to enhance their climate transition models

26 January 2026Forward Analytics partners with Ortec Finance to enhance their climate transition modelsLearn about our partnership with Forward Analytics, as they use the Ortec Finance Climate Scenarios in their forward-looking climate transition models.

-

19 January 2026How climate change could spark an insurability crisis - and destabilize the global financial system

19 January 2026How climate change could spark an insurability crisis - and destabilize the global financial systemLearn how a climate-driven insurability crisis could compromise global financial stability.