Portfolio optimization allows investors to make optimal risk-return trade-offs and plays a crucial role in their investment decision process. Unfortunately, optimal portfolios are sensitive to changing input parameters, i.e. they are not very robust. Traditional robust optimization approaches aim for an optimal and robust portfolio which, ideally, is the final investment decision. In practice, however, portfolio optimization supports the investor’s investment decision process but seldom replaces it.

Near optimal portfolios

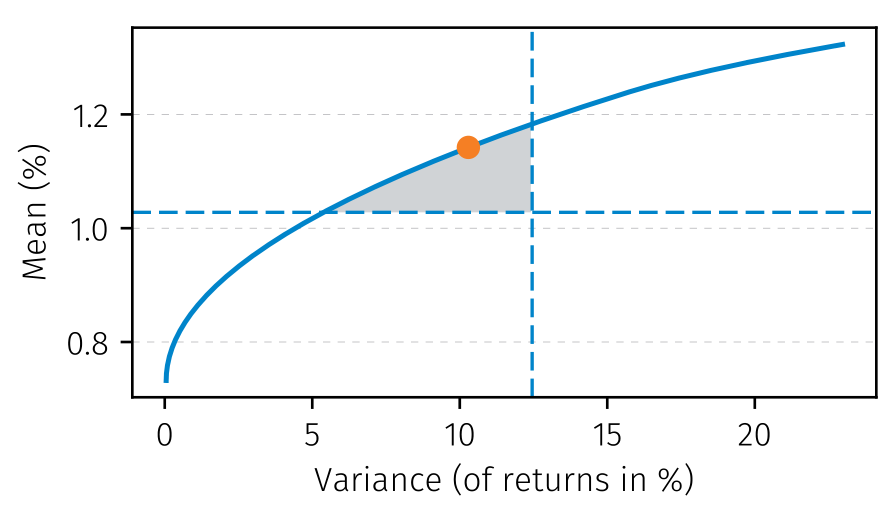

At Ortec Finance, we developed an approach that both solves the robustness problem and aims to support rather than replace the investment decision process. The method determines a region with near-optimal portfolios, i.e., all portfolios in the gray region. In light of the robustness problem, all near-optimal portfolio can be considered good allocation decisions. Then, as is already common practice, an investor can bring in an expert opinion or additional information to select a preferred near-optimal portfolio.

We can show that the region of near-optimal portfolios is significantly more robust than the optimal portfolio itself. Intuitively, this is understandable: with slightly different input parameters, the near-optimal region slightly changes in shape, but most near-optimal portfolios remain near-optimal. For example, the old optimum becomes near-optimal and one of the near-optimal portfolios becomes optimal. For the investor, his allocation becomes more robust, because no revision is needed when it remains near-optimal.

Making better investment decisions

Moreover, the method focusses on supporting rather than replacing the investment decision process. Despite many efforts to make models and optimization problems as realistic as possible by for example incorporating transaction costs, expert opinion and liquidity, a model remains a simplification of reality. The near optimal region allows the investor to choose from many portfolios rather than one portfolio. In the near future, Ortec Finance aims to experiment with and test the added value of this approach. We believe that this method will give investors more insight and that it enables them to make better investment decisions.

Publication in VBA Journaal

VBA Journaal published a paper written by Martin van de Schans about the role of portfolio optimization. Portfolio optimization is the current academic standard for determining an investor’s optimal portfolio. By incorporating future return information and the investor’s goal into the optimization problem, it aims to determine the investor’s optimal investment decision. In the paper is shown how near-optimal portfolios can be used in a new methodology for portfolio construction.

More information?

More information can be found in our working paper. Do you want to know more about portfolio optimization? Feel free to contact Loranne van Lieshout, Marnix Engels or Martin van der Schans.

Contact

Loranne van Lieshout

Teamleader Wealth Management & Decision GuidanceRelated Insights

-

05 February 2026Webinar recording: Performance reporting for advanced analytics: Tools, techniques, and practical guidance

05 February 2026Webinar recording: Performance reporting for advanced analytics: Tools, techniques, and practical guidanceLearn how asset owners can develop a reporting framework that translates complex data, supports manager evaluation and highlights key performance drivers.

-

30 January 2026Webinar recordings: Access past Quarterly Economic Scenario Outlook videos

30 January 2026Webinar recordings: Access past Quarterly Economic Scenario Outlook videosOur webinars dive into the latest economic outlook and tackle the key topics shaping market conditions and investment outcomes.

-

30 January 2026Quarterly Outlook: Q4 2025

30 January 2026Quarterly Outlook: Q4 2025The outlook is based on the Ortec Finance Economic Scenario Generator (ESG) and offers our perspective on recent developments in the economy and capital markets.

-

26 January 2026Forward Analytics partners with Ortec Finance to enhance their climate transition models

26 January 2026Forward Analytics partners with Ortec Finance to enhance their climate transition modelsLearn about our partnership with Forward Analytics, as they use the Ortec Finance Climate Scenarios in their forward-looking climate transition models.

-

23 January 2026Quarterly Pensions Investments Review

23 January 2026Quarterly Pensions Investments ReviewThe Quarterly Pensions Investments Review is a comparison in expected risk and investment return.

-

19 January 2026How climate change could spark an insurability crisis - and destabilize the global financial system

19 January 2026How climate change could spark an insurability crisis - and destabilize the global financial systemLearn how a climate-driven insurability crisis could compromise global financial stability.

-

13 January 2026UK Defined Benefit Pension Schemes: Endgame Strategy Evaluation Using an ALM-Based Approach

13 January 2026UK Defined Benefit Pension Schemes: Endgame Strategy Evaluation Using an ALM-Based ApproachExplore DB pension endgame options beyond buy-out. Compare run-on and captive insurance using an ALM-based approach. Download the whitepaper.

-

08 January 2026Quarterly Scenario webinar Q4 2025 - 'New Year, New Rules? Reassessing the Economic Landscape'

08 January 2026Quarterly Scenario webinar Q4 2025 - 'New Year, New Rules? Reassessing the Economic Landscape'Join us on January 29 for our Q4 webinar for Insightful Market Analysis and Strategy Guidance. Join our in-house experts, Jordan ter Borch, Ben Hudson and Selina Wang, for a 60-minute session unpacking the trends shaping 2026 and the latest strategies for defined benefit (DB) endgames.

-

10 December 2025Translating the cost of climate change for the European insurance industry: 2025 update

10 December 2025Translating the cost of climate change for the European insurance industry: 2025 updateDiscover how climate change is impacting insurance companies across the total balance sheet, using the 2025 Ortec Finance Climate Scenarios