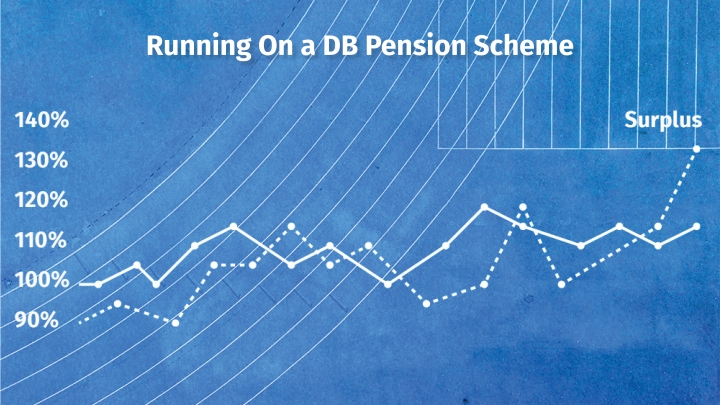

For a pension scheme looking to “run-on”, life will not be too dissimilar to how it has operated thus far – assets will continue to be invested by the scheme, and benefit payments will continue to be met by the scheme when they fall due.

There are however some key factors that Trustees and sponsors need to consider when going down the run-on road...

Surplus extraction:

- As surplus extraction becomes a more probable scenario, the surplus extraction framework will need to be designed, refined, and rigorously tested to provide decisionmakers with a comprehensive view of both upside and downside risks.

Risk exposures:

- Unlike an insurer buy-in/out, the scheme’s funding risks - such as investment risk, longevity risk, governance risk - remain with trustees and sponsors. Ongoing monitoring and mitigation will be essential to effectively manage these risks.

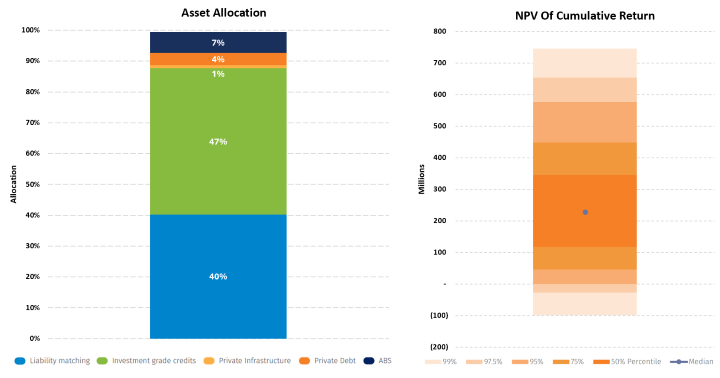

A run-on investment strategy offers flexibility to invest (or continue to invest) in illiquid assets. Risk modelling should be carried out to assess the liquidity required to meet future benefit cashflows. In fact, a cashflow driven type of investment strategy may still be appropriate.

The below illustrates a range of asset classes a scheme can invest in during the run-on period. The list is not exhaustive.

Source: Ortec Finance Scenarios

-

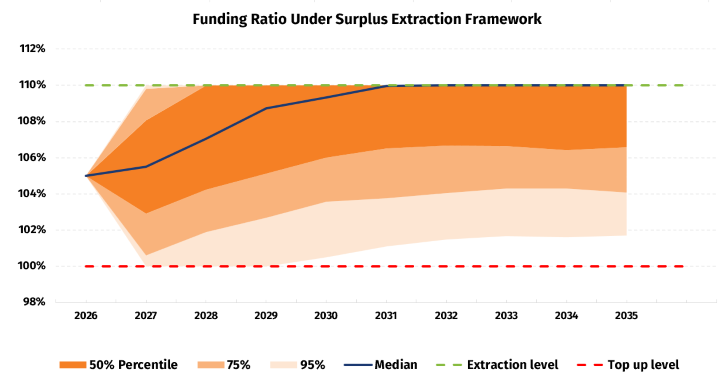

A surplus extraction framework

Extraction level:

- • What will be the measure that triggers the extraction of surplus. This is expected to be a funding level on a particular liability basis such as 110% on the low dependency basis.

- • A further prudent layer could be added such as "average funding level to be above 110% on the low dependency basis over the last 12 months" to allow for market volatility over the period.

Extraction rate:

- • The amount of surplus to be extracted can be set to be simply the excess amount above the extraction point.

- • Equally there could be a simmered approach where "50% of the excess above the extraction point in year 1, 60% of the excess above the extraction point in year 2..." And so on to ensure a buffer is built up to mitigate any downside risks.

Recovery contributions:

- • In the event of funding deterioration, recovery contributions can be built into the framework as a 'top up level' to protect against a growing deficit and ensure the benefits of scheme members.

- • Set up contribution rules to be conditional on the funding position at one specific point in time or based on an average over a specified period.

Surplus sharing:

- • The sponsor can take all of the surplus generated, or share part of the surplus with scheme members via discretionary indexation increases or direct member payments.

In the research paper linked to this blog, we projected forward multiple investment strategies over the next 10 years using stochastic scenarios to observe how they performed in relation to the key metrics that are of interest.

- Scheme: The pension scheme in this study is 105% funded on a low-dependency basis of gilts+0.5% p.a. The liability value is £3bn on the same valuation basis.

- Surplus extraction framework:

- Excess surplus is extracted when the funding ratio is over 110% on the low-dependency basis at the year-end; and

- A lump sum deficit contribution will be made if the funding ratio falls below 100% on the low-dependency basis, to bring the funding level back to 100%.

The charts below show one of the modelled investment strategies and the corresponding results of the cumulative Net Present Value (NPV) of net return (surplus extracted minus deficit contributions). This is a key metric a sponsor should be considering with this type of solution.

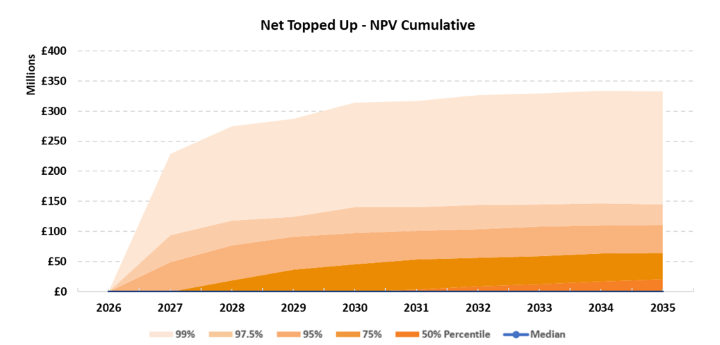

As part of the run-on framework, recovery contributions can be incorporated as an additional line of defense to protect any funding level deterioration. ALM tools can be used to assess the best ‘top-up level’ for a specific scheme and the use of stochastic modelling to understand the probability of requiring these contributions. The chart below shows the Net Present Value of deficit contributions required for a pensions scheme under the investment strategy outlined above.

Given the sensitivity of outcomes to these assumptions-as well as differences in scheme design and stakeholder risk appetite-the results can vary significantly. This highlights the importance of performing a schemespecific stochastic ALM analysis to assess the value of a run-on solution for each case.

Our latest research paper uses GLASS (Ortec Finance’s ALM tool) to dive deeper into the analysis above, comparing multiple risk frameworks.

Interested to know more?

This article is the third in our series on rethinking the endgame for UK defined benefit pension schemes,

Download the whitepaper for a full comparison of endgame options where we evaluate the options using GLASS.

Or access the full series, here

Contact

Ashish Doshi

UK Insurance Lead

Selina Wang

Senior Consultant - Insurance Solutions

Ben Hudson

Senior ConsultantRelated Insights

-

28 July 2026Webinar: Funding ratio attribution for asset owners under higher interest rates

28 July 2026Webinar: Funding ratio attribution for asset owners under higher interest ratesLearn how to develop a funding/solvency attribution framework that encompasses a comprehensive view of the fund’s performance.

-

28 July 2026Ortec Finance selected by Ostrum Asset Management for its GLASS ALM and PRISM Machine-Learning Optimization tools

28 July 2026Ortec Finance selected by Ostrum Asset Management for its GLASS ALM and PRISM Machine-Learning Optimization toolsOrtec Finance, a leading provider of investment modelling solutions, today announced that Ostrum Asset Management, an expert Insurance and Institutional investment manager and affiliate of Natixis Investment Managers, has selected Ortec Finance’s GLASS ALM and PRISM Machine-Learning Optimization solutions to provide an enhanced investment solutions offering to its insurance and pension clients.

-

27 July 2026Top-down or bottom-up? How should institutional investors manage climate risk?

27 July 2026Top-down or bottom-up? How should institutional investors manage climate risk?Evaluate the top-down and bottom-up approaches to managing climate risk and examine which is more effective at improving portfolio resilience

-

22 July 2026Article GLASS PRISM: The Evolution of Insurance Asset Portfolio Optimization

22 July 2026Article GLASS PRISM: The Evolution of Insurance Asset Portfolio OptimizationFollowing the launch of GLASS PRISM, Ortec Finance attracted significant media attention, with industry publications exploring how the solution is transforming portfolio optimization for institutional investors.

-

20 July 2026Articles GLASS PRISM: A New Standard in Strategic Asset Allocation

20 July 2026Articles GLASS PRISM: A New Standard in Strategic Asset AllocationThe GLASS PRISM launch introduces targeted SAA powered by scenario-based machine learning. Discover what's driving industry attention.

-

06 July 2026Quarterly Scenario Webinar Q3 2026 - Energy Shocks and Market Repricing: Navigating the Next Phase

06 July 2026Quarterly Scenario Webinar Q3 2026 - Energy Shocks and Market Repricing: Navigating the Next PhaseJoin our webinar to explore how renewed US–Iran military conflict could reshape energy markets, inflation, interest rates and investment portfolios.

-

18 June 2026Virtual panel discussion #2 (Asia-Pacific): Extending the lens on climate change to capital market assumptions

18 June 2026Virtual panel discussion #2 (Asia-Pacific): Extending the lens on climate change to capital market assumptionsHear thought-provoking perspectives on climate change’s impact on capital market assumptions, including short and longer-term market pricing dynamics

-

18 June 2026TPA Quick Wins Article

18 June 2026TPA Quick Wins ArticleHow to adopt the TPA framework without fully transitioning to TPA.

-

05 June 2026Strategic Asset Allocation in the “TW-ICS” Era

05 June 2026Strategic Asset Allocation in the “TW-ICS” EraHow Taiwanese insurers can modernize strategic asset allocation and strengthen long-term resilience.