Since the implementation of Solvency II there is an ongoing shift in the way in which analysts and other stakeholders look at the financial performance of European insurers. Traditionally, the IFRS accounting framework was the metric of choice in this regard, but stakeholders nowadays are more interested in the development of the solvency ratio and an insurer’s ability for ‘free capital generation’. If an insurer is able to generate a higher amount of free capital, this could translate into either higher dividend payments to shareholders or increased possibilities to make strategic investments or acquisitions. The Dutch regulator also recognizes the importance of this issue. In line with their ‘Vision for the Future of the Dutch Insurance Sector’, they will be asking insurers over the course of 2018 how they intend to generate free capital in the long run.

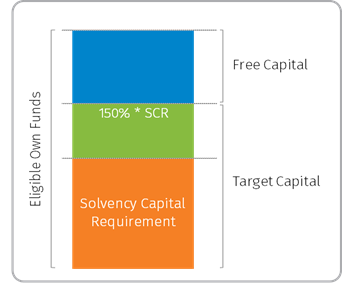

Under Solvency II ‘free capital’ is defined as the amount of Eligible Own Funds in excess of either the regulatory required capital or (to be more prudent) the target capital. The insurers ability for free capital generation is hence defined as the change in the amount of free capital over time excluding dividend payments. The elements underlying free capital generation can be split into two distinct categories: elements that can be considered ‘sustainable’ and elements that are caused by external or unique events. Events that fall into the latter category include for instance changes in regulatory requirements or model changes.

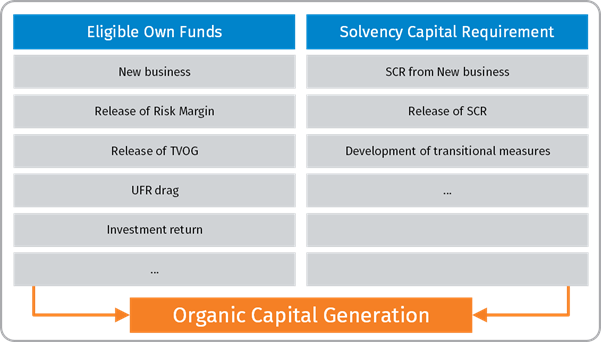

Organic Capital Generation

The most relevant elements of free capital generation are the ones that are considered ‘sustainable’; i.e. unilaterally generated by the insurer. These provide the best insight into the dividend capacity and to some extent the dividend sustainability of the insurer. The capital generation caused by these sustainable elements is also known as ‘organic capital generation’. The figure below gives an overview of the generic sources of organic capital generation for an insurer.

Prospective view on organic capital creation

Insurers are taking action to improve their free capital position by for instance de-risking their asset portfolios or entering into reinsurance contracts. Improving the organic capital creation is essential for a stable development of the solvency ratio and stable dividend payments. However, most of these management actions tend to improve the solvency and free capital position of the insurer in the short term, but deteriorate the profitability of the business in the long run.

It is therefore vital to keep an eye on the long term, as a lack of profitability will diminish the organic capital generation going forward. By gaining insight into the impact of certain management actions beforehand – not only the immediate effect, but also the impact this could possibly have given different (economic) outlooks – the decision to implement such actions can also contribute to stable results going forward. This insight could be easily obtained through forward-looking ALM or risk management analyses. This will create maximum value for all stakeholders not only now but also for years to come.

Related Insights

-

22 July 2026Article GLASS PRISM: The Evolution of Insurance Asset Portfolio Optimization

22 July 2026Article GLASS PRISM: The Evolution of Insurance Asset Portfolio OptimizationFollowing the launch of GLASS PRISM, Ortec Finance attracted significant media attention, with industry publications exploring how the solution is transforming portfolio optimization for institutional investors.

-

20 July 2026Articles GLASS PRISM: A New Standard in Strategic Asset Allocation

20 July 2026Articles GLASS PRISM: A New Standard in Strategic Asset AllocationThe GLASS PRISM launch introduces targeted SAA powered by scenario-based machine learning. Discover what's driving industry attention.

-

06 July 2026Quarterly Scenario Webinar Q3 2026 - Energy Shocks and Market Repricing: Navigating the Next Phase

06 July 2026Quarterly Scenario Webinar Q3 2026 - Energy Shocks and Market Repricing: Navigating the Next PhaseJoin our webinar to explore how renewed US–Iran military conflict could reshape energy markets, inflation, interest rates and investment portfolios.

-

18 June 2026Virtual panel discussion #2 (Asia-Pacific): Extending the lens on climate change to capital market assumptions

18 June 2026Virtual panel discussion #2 (Asia-Pacific): Extending the lens on climate change to capital market assumptionsHear thought-provoking perspectives on climate change’s impact on capital market assumptions, including short and longer-term market pricing dynamics

-

18 June 2026TPA Quick Wins Article

18 June 2026TPA Quick Wins ArticleHow to adopt the TPA framework without fully transitioning to TPA.

-

05 June 2026Strategic Asset Allocation in the “TW-ICS” Era

05 June 2026Strategic Asset Allocation in the “TW-ICS” EraHow Taiwanese insurers can modernize strategic asset allocation and strengthen long-term resilience.

-

05 June 2026Total Portfolio Lens Brochure

Total Portfolio Lens (TPL) is built for investors navigating whole-fund complexity: it connects forward-looking analytics to action and allows investors to evolve at a pace that fits their governance and readiness.

-

01 June 2026Ortec Finance publishes its first Sustainability report

01 June 2026Ortec Finance publishes its first Sustainability reportOrtec Finance publishes its first Sustainability Report. It covers the reporting years 2024 and 2025.

-

28 May 2026Captive Insurance vs Run-On: What Do the Numbers Say?

28 May 2026Captive Insurance vs Run-On: What Do the Numbers Say?In blog 6 in the series, we look at some specific case studies to highlight how alternative endgame arrangements can deliver meaningful financial benefits for both sponsors and members.