One of the main challenges within the field of performance measurement is to provide analyses that are recognizable and understandable for the target audience. The returns that are calculated and presented should match the official returns that people recognize and accept. For a portfolio this could be the return based on published NAV’s or the returns as calculated by an external party. For benchmarks the returns are expected to match the officially published index returns.

Providing insightful analyses

An insightful analysis generally requires more granular information. Consider for example an analysis that is intended to show the impact of currency movements on the total excess return, and to provide insight in the added value of the management of the different currencies. For such an analysis information on the currency distribution within the portfolio and the benchmark is required. Another example is an analysis that provides insight in the largest contributors to the total performance, on an absolute basis or relative against a benchmark.

The granular information is often available on security level. Returns are calculated for different levels of the analysis by grouping together the securities based on their properties, e.g. country or sector classification. On the total level, the returns that are calculated bottom-up from the security level are generally not exactly the same as the official return numbers. The reasons for the differences are often easily explainable and out of the control area of the performance analyst responsible for the analysis. Therefore these differences are often considered as something that they simply have to live with: the ability to provide more detailed analyses based on security level data comes with the drawback that on a total level the returns do not match the official portfolio or benchmark returns.

Solutions

The industry has come up with two solutions for this problem. The first is that you can smooth the difference between the bottom-up calculated return and the official return by changing the returns and weights of the securities slightly. This approach requires a smoothing algorithm which is often not straightforward to implement and difficult to explain. Therefore this solution is not commonly used.

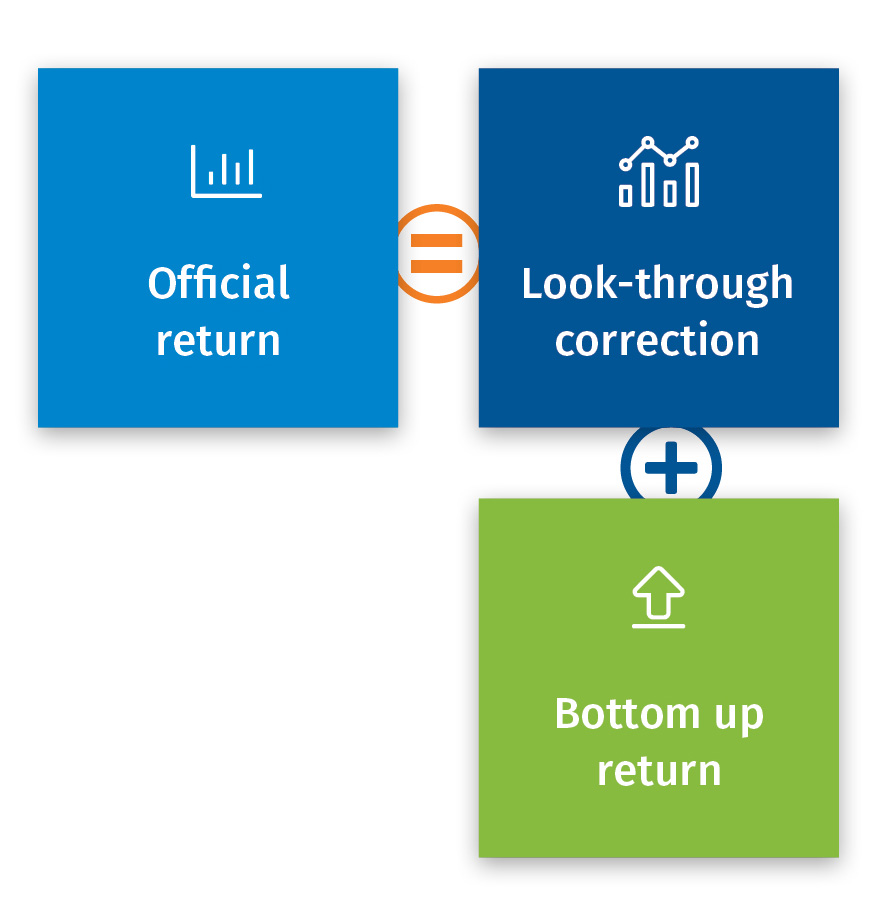

An alternative and often preferred solution is to apply look-through from the official portfolio or index (one-liner) to the underlying security level information. In this solution the security weights and returns are not artificially changed, but a separate correction position is created that contains the difference between the bottom-up and official returns. This look-through correction can be shown separately in an analysis, since it provides insight in the data quality. Alternatively it can also be included in one of the segments in the analyses.

Being creative with look-through

The quality of a detailed analysis can be enhanced by creatively configuring look-through relations and carefully labelling the resulting corrections. Let’s explain this with an example. Consider a portfolio having a currency hedged index as its official benchmark. As the portfolio performance is measured against a hedged index, the portfolio manager is also expected to hedge the currency risk in the portfolio. The hedging methodology that is used by the index provider to calculate the hedged index could well differ from the implemented currency hedge in the portfolio. The index provider typically does not provide the contribution to the total hedge result of each of the securities in the index. By configuring a look-through relationship between the hedged index and the underlying constituents, the look-through solution would not only correct for the difference between the bottom-up calculated return and the official index return, but it would also include the hedging impact.

To separate the hedging and the data quality impact, a two-level look-through can be used:

1. A look-through relation from the hedged index to the unhedged index.

2. A look-through relation from the unhedged index to the bottom-up calculated return.

With this configuration two corrections would be calculated for the benchmark, the first being the correction of the hedging methodology and the second the correction for the difference between the bottom-up calculated return and the official return. The first contribution can be labeled as the currency management impact, whereas the second would be labeled as a data quality impact.

Conclusion

To conclude, using look-through allows for reporting on official, recognizable and understandable returns, also in detailed analyses. The look-through correction position offers additional insights, and as such is a valuable addition to the toolset of the performance measurement specialist.

PEARL is used by a growing number of leading asset owners and asset managers worldwide. Get more from your performance reporting, and let PEARL help you to enhance your performance and master the complexity of investment decision making. Click here to find out more about PEARL.

Contact

Bas Leerink

Head of Global Implementations Investment PerformanceRelated Insights

-

05 June 2026Strategic Asset Allocation in the “TW-ICS” Era

05 June 2026Strategic Asset Allocation in the “TW-ICS” EraHow Taiwanese insurers can modernize strategic asset allocation and strengthen long-term resilience.

-

05 June 2026Total Portfolio Lens

05 June 2026Total Portfolio LensTotal Portfolio Lens (TPL) is built for investors navigating whole-fund complexity: it connects forward-looking analytics to action and allows investors to evolve at a pace that fits their governance and readiness.

-

01 June 2026Supporting PKZH in assessing the financial impact of an ESG exclusion policy using PEARL

01 June 2026Supporting PKZH in assessing the financial impact of an ESG exclusion policy using PEARLLearn how we supported PKZH, a Swiss pension fund in understanding the effect of an ESG exclusion policy on total fund performance.

-

01 June 2026Ortec Finance publishes its first Sustainability report

01 June 2026Ortec Finance publishes its first Sustainability reportOrtec Finance publishes its first Sustainability Report. It covers the reporting years 2024 and 2025.

-

28 May 2026Captive Insurance vs Run-On: What Do the Numbers Say?

28 May 2026Captive Insurance vs Run-On: What Do the Numbers Say?In blog 6 in the series, we look at some specific case studies to highlight how alternative endgame arrangements can deliver meaningful financial benefits for both sponsors and members.

-

19 May 2026Total Portfolio Lens

This report introduces two closely related concepts that fill the gap between traditional SAA and full TPA.

-

13 May 2026Webinar recording: TPA Quick Wins

13 May 2026Webinar recording: TPA Quick WinsThis webinar explores TPA quick wins – practical steps that can be taken within existing frameworks to start capturing the benefits of TPA.

-

08 May 2026Quarterly Pensions Investments Review

08 May 2026Quarterly Pensions Investments ReviewThe Quarterly Pensions Investments Review is a comparison in expected risk and investment return.

-

07 May 2026Rethinking the Endgame for UK Defined Benefit Pension Schemes

Rethinking the Endgame for UK Defined Benefit (DB) Pension Schemes – Explore our blog series and discover how leading schemes are navigating the changing landscape.