As part of the regulator’s effort to improve Australia’s superannuation industry’s efficiency, transparency and accountability, the Government’s Your Future, Your Super reforms (the YFYS reforms) came into effect on 1 July 2021. It came to our attention that there has been increasing demand in our client base to build the performance test analysis internally, as requested by various stakeholders within the organization.

We believe there is value-add in sharing some of our learning, experience, and reflections we gained throughout the journey, through this series of two insights. In this first article today, we reflect on some of the practical challenges we have seen in building the calculation of the performance test itself. In the upcoming episode, we will go a step further and look at what kind of narrative can be derived from the performance test via attribution analysis.

The YFYS Performance Test

Under the YFYS reform, APRA is required to conduct an annual performance test for MySuper products (later on to be extended to Choice products) offered by superannuation companies, by comparing the fund’s 8-year rolling annualized return against APRA’s Strategic Asset Allocation (SAA) benchmark. A fund can fail the performance tests if it underperforms by more than 50bps.

Consequences of failing the test are significant. It involves sending a standard letter to its members to inform them of this result. If failing two consecutive years in a row, the fund will not be allowed to accept new members until their net investment performance improves.

The merits and demerits of the YFYS Performance test have been hotly debated amongst investment professions in various forums via articles, papers, interviews, and conferences. Whilst these conversations are still happening, there has been an increasing demand for performance teams to calculate the performance test internally, for obvious reasons, for example:

- To shadow APRA’s calculation

- To track fund’s performance and alert internal stakeholders if the fund gets close to failing the test

- To produce performance test forecast and conduct what-if and scenario analysis

- To perform attribution analysis which may help answer the question: what can be done to improve the test result.

The devil is in the details

Performance team’s initial attempt to create the performance test typically starts in Excel – the ultimate template tooling, with a combination of Excel add-ins for sourcing data, such as Power Query, APIs and Add-ins from various market data vendors or data warehouses.

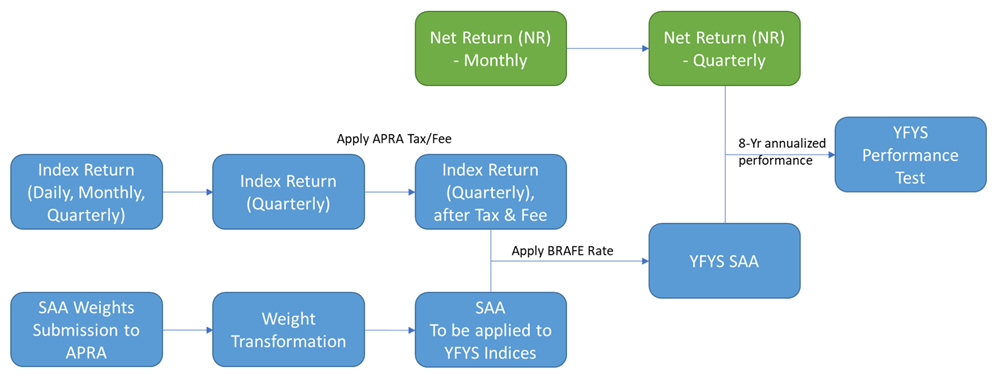

The calculation of the performance test itself is relatively straight-forward. It can be summarized with the flow chart below. However, when going through the exercise of creating the performance test, we observed quite a few nitty-gritty aspects of the calculation that may worth extra attention.

For example, sourcing of benchmark data and preparing for index return calculation may seem straightforward but typically can be quite tricky to handle in Excel. Most of the APRA benchmarks are daily series when coming from benchmark providers, with the exceptions of the quarterly indices for unlisted asset classes. The availability of the benchmark data for the unlisted could result in delayed/lagged data points.

If there is a requirement to calculate the performance test with a higher frequency than quarterly, interpolation might also be necessary for quarterly indices. Another important task, as part of the journey, is to transform the SAA weights submitted to APRA so that they can be applied to the YFYS indices. Complications can arise when:

- Hedging policy is designed at Option level but specified at asset class level in YFYS performance test. APRA has now provided field for supers to submit the hedging ratio at option level and treat currency overlay as a separate asset class. However, the benchmark to be assigned to the currency overlay asset class is still unclear at this stage

- Assumptions made by APRA when domestic/international split is not provided by the fund/not available

- Mapping of internal asset class classifications to APRA asset class classification and the management of historical change over time.

In addition, an audit to review all historical SAA weights submitted to APRA must be conducted to make sure they are accurate.

These considerations add to the complexity of the APRA performance test model built in Excel. Furthermore, there is the element of key-person risk associated with any manually developed Excel template. With the help of a system, embedding a stronger data governance framework coupled with more robust tooling capability, it could help the performance team to manage the requests of analysis in relation to performance test, in a much more efficient and effective way.

What have we done in PEARL

When we looked at creating the performance test in PEARL, we have spent quite some time going through discussions with our clients and contacts to understand their pain points when producing the analysis. We then designed our solution and workflow focused on:

- Minimizing data sourcing effort, including but not limited to, APRA indices return, fees/tax/BRAFE rate, fund asset class level returns which may be required for attribution analysis

- Ease of maintaining APRA assumptions like fees/tax rate through one single configuration allowing changes over time

- Maximizing the efficiency by creating asset class building blocks, allowing for scalability when the test is extended to Choice products

- Flexibility in dealing with delay/lagging/interpolation requirements for quarterly indices

- Allowing for residuals to be quantified, which could arise due to data availability and data quality and calculation frequency.

From Performance Test to Performance Test Attribution

So now you have got the performance test, what now? The next step, which intuitively comes to mind is, indeed, in the attribution. In the context of the YFYS performance test, the attribution framework should provide insights and guidance in terms of what needs to be done to avoid failing the performance test, assess asset class teams and investment managers fairly, and bring the best outcomes to the members. One can and should expect logical flow and consistency between the performance test and the results of the decision attribution analysis. We started exploring an attribution framework intended to measure and quantify impact for several decisions:

- Designing the hedging policy and its implementation – understanding the asset class contributors/detractors relative to the APRA benchmarks

- Determining the admin fee rate

- Managing the tax efficiency

- Selecting funds’ strategic SAA benchmarks which deviates from APRA SAA benchmarks.

In the next episode of this series, we will deep dive into an example of the YFYS performance test attribution and see what kind of insights we may get, and challenges we may run into. Stay tuned.

Contact

Michelle Li

Head of Client Services APAC & Head of AustraliaRelated Insights

-

19 February 2026Evaluating performance with attribution based on the investment decision process

19 February 2026Evaluating performance with attribution based on the investment decision processExplore how our proprietary IDP model enables asset owners to evaluate performance with attribution based on the investment decision-making process

-

18 February 2026Breaking down the Bank of England Prudential Regulation Authority’s guidance on the management of climate-related risks for UK insurers

18 February 2026Breaking down the Bank of England Prudential Regulation Authority’s guidance on the management of climate-related risks for UK insurersExplore the BoE’s expectations on how UK insurers should manage climate risks across their balance sheets and embed them into risk management frameworks

-

18 February 2026The Investment Decision Process (IDP) model: From inception to a legacy of innovation

18 February 2026The Investment Decision Process (IDP) model: From inception to a legacy of innovationDiscover how the Investment Decision Process model was developed and how it helps asset owners understand the impact of each decision on total fund return

-

05 February 2026Webinar recording: Performance reporting for advanced analytics: Tools, techniques, and practical guidance

05 February 2026Webinar recording: Performance reporting for advanced analytics: Tools, techniques, and practical guidanceLearn how asset owners can develop a reporting framework that translates complex data, supports manager evaluation and highlights key performance drivers.

-

30 January 2026Webinar recordings: Access past Quarterly Economic Scenario Outlook videos

30 January 2026Webinar recordings: Access past Quarterly Economic Scenario Outlook videosOur webinars dive into the latest economic outlook and tackle the key topics shaping market conditions and investment outcomes.

-

30 January 2026Quarterly Outlook: Q4 2025

30 January 2026Quarterly Outlook: Q4 2025The outlook is based on the Ortec Finance Economic Scenario Generator (ESG) and offers our perspective on recent developments in the economy and capital markets.

-

26 January 2026Forward Analytics partners with Ortec Finance to enhance their climate transition models

26 January 2026Forward Analytics partners with Ortec Finance to enhance their climate transition modelsLearn about our partnership with Forward Analytics, as they use the Ortec Finance Climate Scenarios in their forward-looking climate transition models.

-

23 January 2026Quarterly Pensions Investments Review

23 January 2026Quarterly Pensions Investments ReviewThe Quarterly Pensions Investments Review is a comparison in expected risk and investment return.

-

19 January 2026How climate change could spark an insurability crisis - and destabilize the global financial system

19 January 2026How climate change could spark an insurability crisis - and destabilize the global financial systemLearn how a climate-driven insurability crisis could compromise global financial stability.