This is a second episode of the YFYS performance test series focusing on extending the YFYS performance test to attribution analysis to see what kind of insights we could potentially gain through a simple case study.

In the first episode of the YFYS performance test series (access here), we discussed the practical challenges when attempting to recreate the calculation of the YFYS performance test internally, as well as what PEARL could help you with some of these challenges.

Once you have the test up and running internally, you might be wondering, or, get asked by internal stakeholders, why the fund is over/under performing the APRA benchmark? This is where attribution analysis might be able to help you:

- To understand asset class contributors/detractors relative to the APRA benchmarks

- To assess the success of the hedging policy and its implementation

- To evaluate the admin fee rate in comparison with BRAFE rate

- To appraise how effectively the tax has been managed per asset class

- To weigh up the impact of selecting funds’ strategic SAA benchmarks that deviates from APRA SAA benchmarks.

In this article, we will first discuss additional data requirements for attribution analysis, followed by a case study (based on dummy data) to illustrate an example of how attribution may help with decision making.

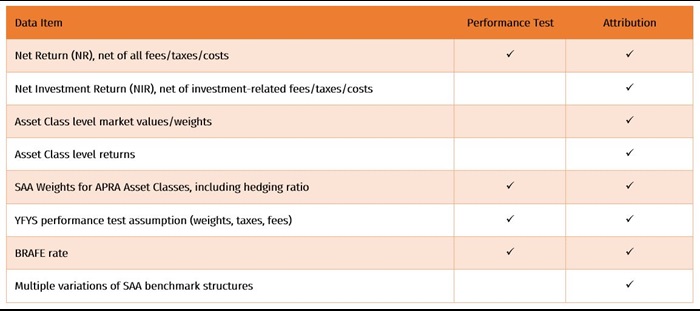

Additional Data Sets required for Attribution Analysis

The table below summarizes the data required for the performance test and additional inputs that can be used in the attribution model.

Additional data for the attribution analysis creates more challenges:

- Require returns at asset class/sector level

To create attribution breakdown to asset classes, weights and returns at asset class levels are required. Typically, these can be sourced from custodian or calculated internally via a P&A system. The type of returns that are available at asset class level could vary or be limited. Net-of-fee or net-of-tax return with investment-related fees/taxes already deducted at sector level are commonly seen available across our clients. Unit Price returns could also be used if various levels of the fund hierarchy are unitized.

Reconciliation between bottom-up asset class returns v.s. NIR A small difference between a bottom-up calculated return from asset classes and the top-level NIR/NR is commonly seen due to differences in methodology and data quality. The size of the residual should be quantified in the attribution analysis. - Currency Overlays at Option level

In the performance test, open currency exposure is only allowed for International Equity asset class. In practice, a currency overlay programme is more likely to be managed at the option level to achieve the total fund strategic currency targets. In our attribution, we can take the currency decision out from the market implementation by using virtually hedged return at asset class level for attribution breakdown. - Attribution over a longer period (8-year/since inception)

The performance test is done over an 8-year (or since inception) horizon. To perform an attribution analysis over a long period, all the underlying data have to be available over this horizon, which could lead to additional challenges such as poor data quality, data inconsistency, managing historical changes in asset class structures and/or currency hedging strategies, etc.

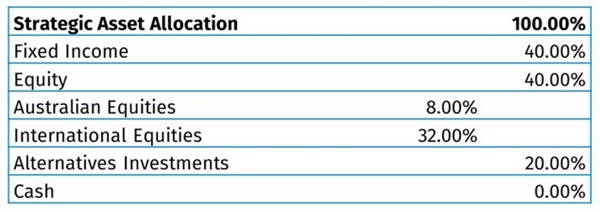

A Case Study

Let us have a look at a very simple example: MySuper Option with the following Strategic Asset Allocation:

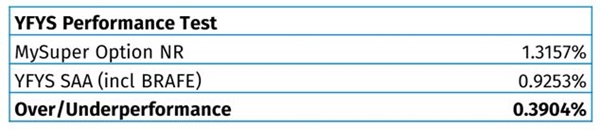

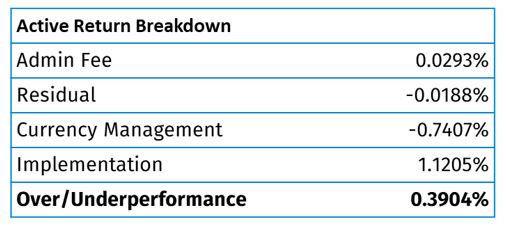

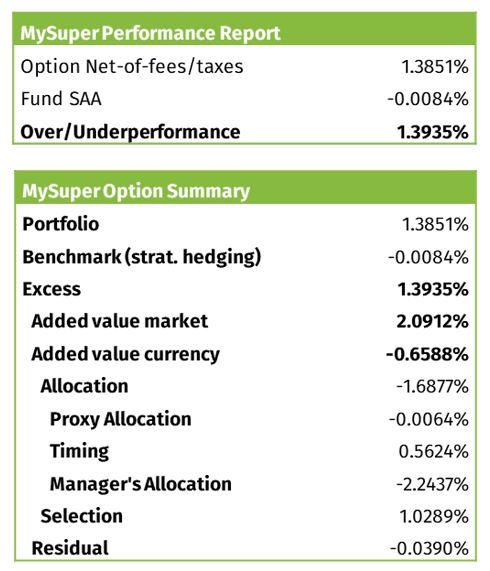

MySuper Option outperforms the YFYS SAA benchmark by 39bps this year. In this example, we are only looking at 1-year of dummy data for the purpose of illustration.

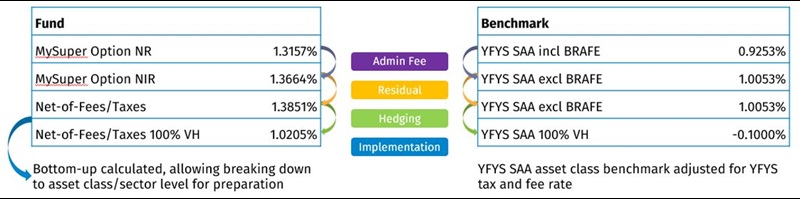

To get ready for the attribution, we are introducing more data and benchmark structures as shown in the table below:

- Starting Point is the YFYS performance test active return of 39bps, which is the total active return we are trying to explain through this attribution analysis.

- Admin fee effect can be evaluated by comparing the impact of the admin fee on the fund side (Net Return – Net Investment Return) and that of the BRAFE rate on the benchmark side.

- Residual impact is quantified by comparing Net Investment Return against a bottom-up calculated net-of fees net-of-taxes return.

- Hedging effect is separated by moving both the fund and benchmark side to 100% virtually hedged (VH), bottom-up calculated net-of fees and taxes return. This is to recognize that the currency hedging of this option is done via the currency overlay program.

- Implementation effect can then be calculated by comparing 100% virtually hedged asset class return against the benchmark.

With the help of the decomposition discussed above, we managed to attribute the total 39bps active return to four components as below:

From the breakdown, one can observe that although the fund did outperform the YFYS benchmark by 39bps with Implementation adding 1.12%, currency hedging dragged the performance by 74bps, which may require further investigation.

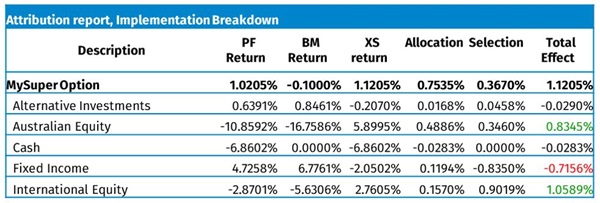

Furthermore, we can utilize a Brinson style attribution to further decompose the overall impact from implementation through an asset class breakdown using fully notionally hedged return on both the portfolio and the benchmark side.

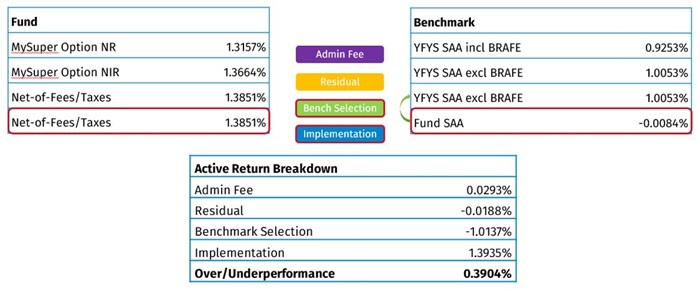

Extension to the Case Study – when fund SAA deviates significantly from APRA SAA

It might be the case when your fund’s official SAA is quite different from APRA SAA, in which case it would be unfair to evaluate how well your managers implemented the strategy by comparing their performance against APRA benchmark because that is not what is given in the mandate. In this case, it may be worth to introduce a benchmark selection effect by comparing the APRA SAA against the Fund SAA – this is the impact of the decision to deviate from the APRA benchmarks.

Of course, this benchmark selection effect can be further decomposed to asset class level to provide further insights:

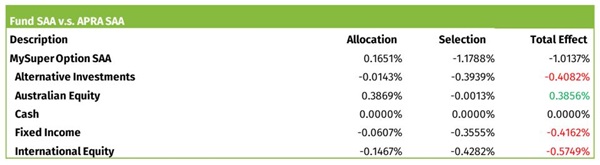

- Majority of the impact, as expected, should be coming from the selection effect, because both SAA benchmarks should be based on the same set of SAA weights.

- Allocation effect would still be present but should be minimal, which could be due to things like rebalancing frequency.

The actual implementation effect, or the active return between the bottom-up Option returns against fund SAA, can be further decomposed to decisions from currency overlay and market implementation (ex-currency overlay) as below.

For more information on Currency Overlay Attribution, please refer to the insight Currency Overlay Attribution: A Practical Guide.

Summary and Reflection

We have discussed why attribution may be useful in providing further insights to the YFYS performance test and demonstrated a simple example of how the attribution could potentially be done via a case study. As an ex-post analysis, attribution can still provide analysis on whether certain factors consistently contribute to or drag the performance, and hence offers input for forward-looking decision-making.

The attribution technique that could be applicable for your situation will vary depending on the specific strategies implemented, how well the fund is tracking the regulatory benchmarks and what kind of story you are looking to tell. However, this could also be limited by whether you have sufficient data and analytic tool that can provide the depth of granularity to enable the story telling. With additional data, the attribution analysis can also be further expanded to evaluate other factors such as tax management per asset class.

Contact

Michelle Li

Head of Client Services APAC & Head of AustraliaRelated Insights

-

30 July 2026Ortec Finance appoints Sam Radford as Head of UK&I Clients

30 July 2026Ortec Finance appoints Sam Radford as Head of UK&I ClientsOrtec Finance names Sam Radford, CFA Head of UK&I Clients in its Global Wealth Solutions team, driving OPAL growth across the UK and Ireland.

-

28 July 2026Webinar: Funding ratio attribution for asset owners under higher interest rates

28 July 2026Webinar: Funding ratio attribution for asset owners under higher interest ratesLearn how to develop a funding/solvency attribution framework that encompasses a comprehensive view of the fund’s performance.

-

27 July 2026Top-down or bottom-up? How should institutional investors manage climate risk?

27 July 2026Top-down or bottom-up? How should institutional investors manage climate risk?Evaluate the top-down and bottom-up approaches to managing climate risk and examine which is more effective at improving portfolio resilience

-

18 June 2026Virtual panel discussion #2 (Asia-Pacific): Extending the lens on climate change to capital market assumptions

18 June 2026Virtual panel discussion #2 (Asia-Pacific): Extending the lens on climate change to capital market assumptionsHear thought-provoking perspectives on climate change’s impact on capital market assumptions, including short and longer-term market pricing dynamics

-

18 June 2026TPA Quick Wins Article

18 June 2026TPA Quick Wins ArticleHow to adopt the TPA framework without fully transitioning to TPA.

-

01 June 2026Supporting PKZH in assessing the financial impact of an ESG exclusion policy using PEARL

01 June 2026Supporting PKZH in assessing the financial impact of an ESG exclusion policy using PEARLLearn how we supported PKZH, a Swiss pension fund in understanding the effect of an ESG exclusion policy on total fund performance.

-

01 June 2026Ortec Finance publishes its first Sustainability report

01 June 2026Ortec Finance publishes its first Sustainability reportOrtec Finance publishes its first Sustainability Report. It covers the reporting years 2024 and 2025.

-

19 May 2026TPL: A New Frontier for Holistic Risk Management

This report introduces two closely related concepts that fill the gap between traditional SAA and full TPA.

-

13 May 2026Webinar recording: TPA Quick Wins

13 May 2026Webinar recording: TPA Quick WinsThis webinar explores TPA quick wins – practical steps that can be taken within existing frameworks to start capturing the benefits of TPA.