Insurance companies issue guarantees that need to be valued according to option prices which capture market expectations. Moreover, for asset liability management and regulation purposes, insurers also need future values of these guarantees. The current common practice is to assume that the option implied volatilities remain constant when calculating future values. It is, however, well-known that these implied volatilities are not constant over time but depend on the state of the economy.

At Ortec Finance, we developed an approach that is able to determine future values of guarantees without assuming constant implied volatilities over time. Instead, the option market is driven by real-world indicators such as the VIX index and interest rates. By including these indicators, we are able to capture important stylized facts of the option market, for example, the implied volatility in the market increases during a financial crisis. These stylized facts will lead to more accurate estimations of future guarantee values.

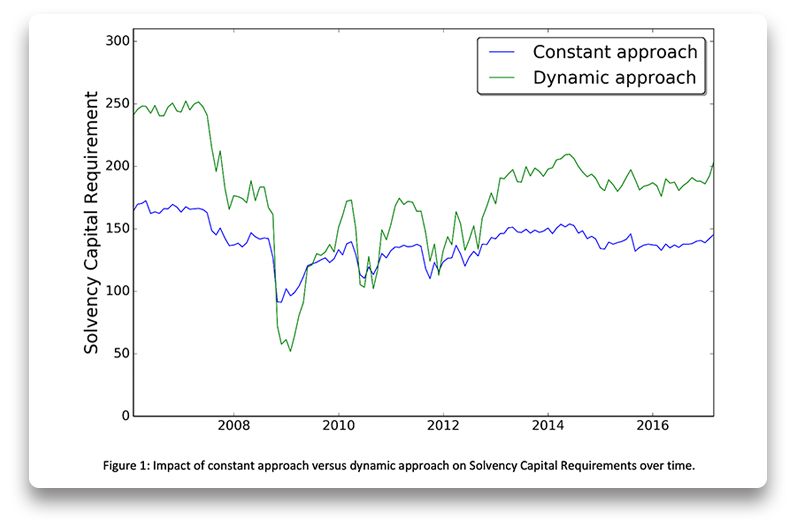

As an example, we demonstrate the impact of the approach on Solvency Capital Requirements. Compared to the constant implied volatility approach, the impact of the dynamic approach on the Solvency Capital Requirements varies between -46% to +52%, see Figure 1. More information on this topic can be found in our publication.

Related Insights

-

27 July 2026Top-down or bottom-up? How should institutional investors manage climate risk?

27 July 2026Top-down or bottom-up? How should institutional investors manage climate risk?Evaluate the top-down and bottom-up approaches to managing climate risk and examine which is more effective at improving portfolio resilience

-

22 July 2026Article GLASS PRISM: The Evolution of Insurance Asset Portfolio Optimization

22 July 2026Article GLASS PRISM: The Evolution of Insurance Asset Portfolio OptimizationFollowing the launch of GLASS PRISM, Ortec Finance attracted significant media attention, with industry publications exploring how the solution is transforming portfolio optimization for institutional investors.

-

20 July 2026Articles GLASS PRISM: A New Standard in Strategic Asset Allocation

20 July 2026Articles GLASS PRISM: A New Standard in Strategic Asset AllocationThe GLASS PRISM launch introduces targeted SAA powered by scenario-based machine learning. Discover what's driving industry attention.

-

13 July 2026Will advisers have to reposition annual reviews as a premium service to justify their fees?

13 July 2026Will advisers have to reposition annual reviews as a premium service to justify their fees?Can advisers still justify ongoing fees without annual reviews? The FCA's shift may reshape advice business models.

-

09 July 2026Aviva partners with Ortec Finance to expand access to financial advice

09 July 2026Aviva partners with Ortec Finance to expand access to financial adviceAviva has selected Ortec Finance as its technology partner to enhance its customer guidance and financial planning proposition.

-

06 July 2026Quarterly Scenario Webinar Q3 2026 - Energy Shocks and Market Repricing: Navigating the Next Phase

06 July 2026Quarterly Scenario Webinar Q3 2026 - Energy Shocks and Market Repricing: Navigating the Next PhaseJoin our webinar to explore how renewed US–Iran military conflict could reshape energy markets, inflation, interest rates and investment portfolios.

-

18 June 2026Virtual panel discussion #2 (Asia-Pacific): Extending the lens on climate change to capital market assumptions

18 June 2026Virtual panel discussion #2 (Asia-Pacific): Extending the lens on climate change to capital market assumptionsHear thought-provoking perspectives on climate change’s impact on capital market assumptions, including short and longer-term market pricing dynamics

-

18 June 2026TPA Quick Wins Article

18 June 2026TPA Quick Wins ArticleHow to adopt the TPA framework without fully transitioning to TPA.

-

05 June 2026Strategic Asset Allocation in the “TW-ICS” Era

05 June 2026Strategic Asset Allocation in the “TW-ICS” EraHow Taiwanese insurers can modernize strategic asset allocation and strengthen long-term resilience.