Goal Priorities in Multi-Goal Based Planning

As financial advice shifts more and more to a client-centric approach, financial goals of clients are becoming increasingly important. Driven by regulations, bank and wealth managers must ensure the product they are selling matches the goals of their clients. In many cases, they use a ‘one pot – one goal’ strategy, determining one specific financial goal for each investment account. However, this is often not the reality. In many cases, especially in the private banking segment, an investor wants to achieve multiple goals with their current and future wealth. To provide the most fitting advice and fully adopt a goal-based approach, all the goals and priorities of the client should be taken into account. This can become a complex process, due to different timing of goals and the relative goal priorities.

For example, consider an investor, Mr Smith, who has one investment account that is designated for two different future goals. Mr Smith would like to buy a beach house in 2025 (priority ***), but he would also like to retire early, in 2030 (priority *****). Early retirement is his most important goal, while the beach house would be a nice extra. In other words, buying a beach house in 2025 should not jeopardize his early retirement. Because of the uncertain development of his capital, we do not know for sure if it is possible to buy the beach house in 2025 if he wants to retire in 2030.

Prioritizing goals

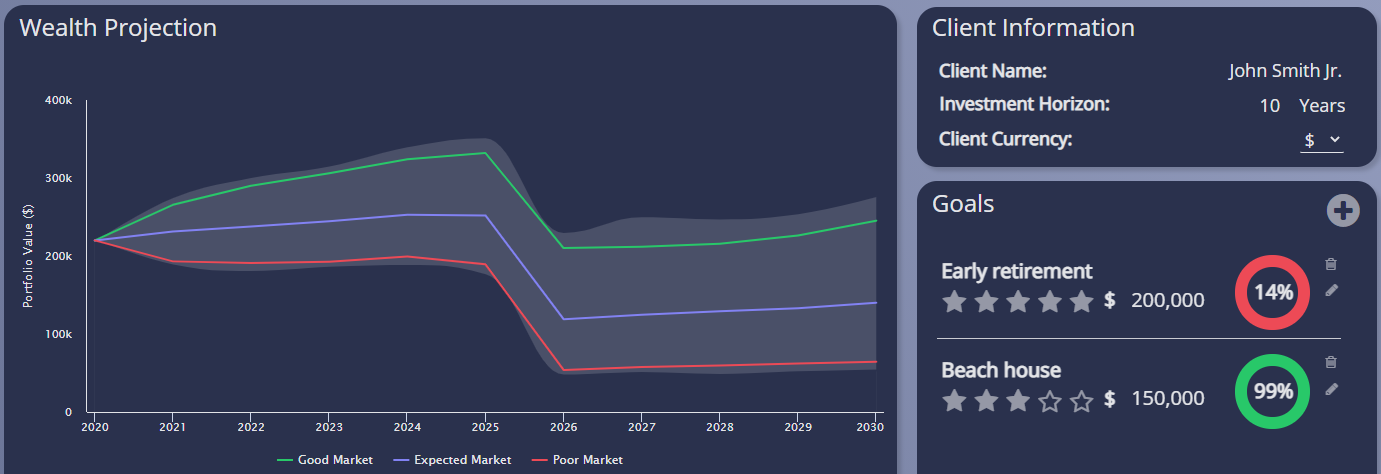

A commonly used method when advising for multiple goals is to use a static simulation for future growth of the capital and finance the goals as they happen over time. If there is enough capital to buy a beach house in 2025, the funds will be spent, no matter the effect on the goal later in time. A simulation of the capital under this assumption could look as follows:

Minimum reservation and expected budget

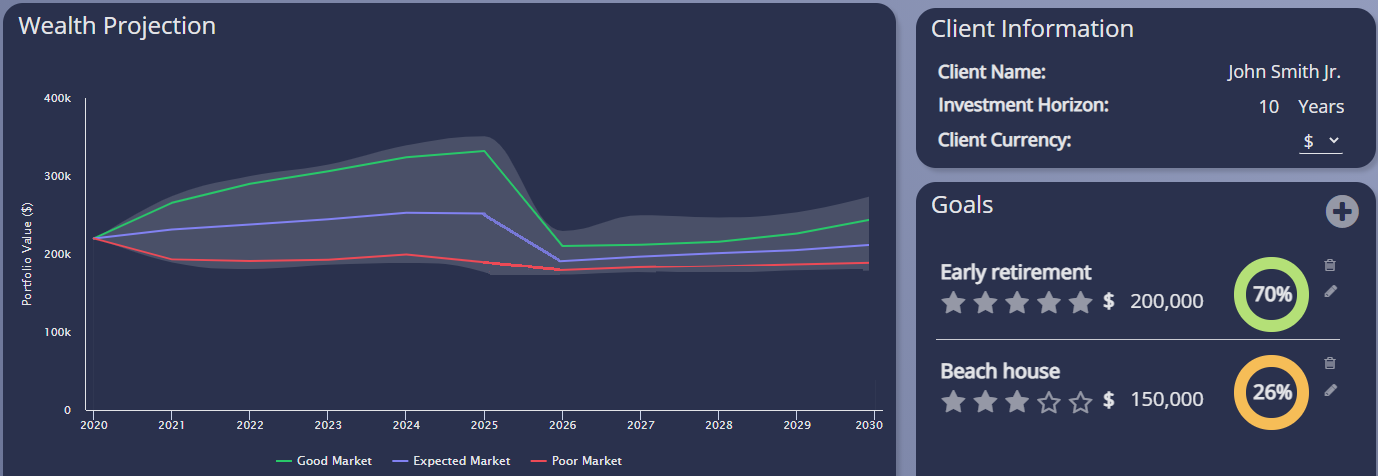

We will look at a strategy that is closer to what Mr Smith will most likely do in reality: he will only spend money on a beach house if this still gives him a high enough chance to realise his early retirement goal. To ensure that the retirement goal remains realistic, we should determine a minimum reservation. This reservation should be left in the account in 2025, after buying the beach house. For example, based on a number of simulations we can determine the minimum reservation in 2025, such that there is a probability of 70% that the early retirement goal is reached. Any capital above that minimum reservation can be spent on the beach house. This means that the budget for the beach house will vary, depending on the performance of the investments up until 2025. A simulation of the capital, when applying this strategy, could look as follows:

As an advisor, there are two major insights that you can provide your client based on this strategy. The first insight would be the minimum reservation of capital that should be left on the account to ensure the feasibility of a high priority goal. The second insight shows the expected budget that can be spent on a low(er) priority goal.

For example, in the case of Mr Smith, he originally wanted to buy a beach house worth € 150.000. As a result of the simulation, the advisor shows that he will need a minimum reservation in 2025 of € 200.000 to ensure his early retirement in 2030. Under expected market conditions, Mr Smith might be able to spend only € 90.000 on the beach house. However, when a poor economic scenario occurs and the investment portfolio generates a low or even negative return, Mr Smith might not be able to spend any money on a beach house. This is because in this scenario his account does not have €200.000 in 2025. If market conditions are favourable, Mr Smith might be able to spend the desired full amount of € 150.000.

Showing insights into the expected budget for the beach house in different economic market conditions is valuable information for the client, and provides a clear view of what to expect for both of his goals.

Monitoring insights and advice over time

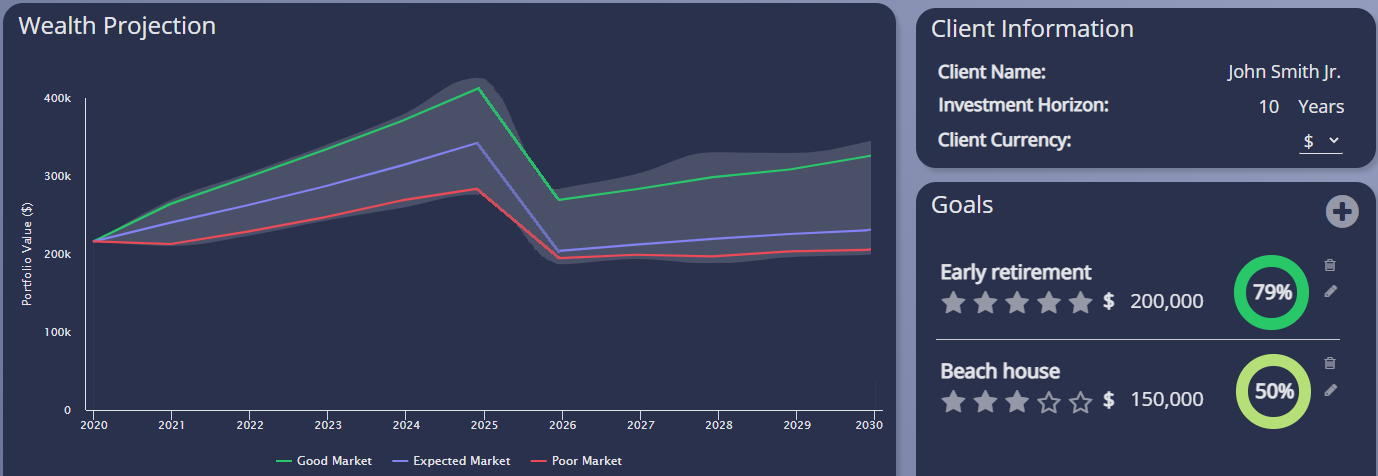

In the strategy described above, an important aspect is that the investor has to take the minimum reservation for the highest priority goal into account, when spending money on the first goal. Because market conditions change, it is very important to monitor the results over time and to adjust the plan in case minimum reservations change. The closer the investor gets to his first goal, the better he can determine the exact minimum reservation that needs to remain in his account for the second goal.In the case of Mr Smith, he might not be satisfied with the low feasibility for his beach house goal. In order to improve the chances of reaching this goal, there are multiple steering variables he can use, like changing his risk profile, redefining his goal, or increase his monthly savings. For example, a monthly saving of € 1.000 increases the feasibility of his beach house to 50%. A simulation of the capital, when applying this strategy, could look as follows:

The additional savings have also improved the feasibility for the early retirement goal. Even without the additional savings, Mr Smith knows that he can most likely achieve his early retirement. This means that he can make a personal assessment if saving on a monthly basis is something he wants to do in order to buy the beach house.

Improve advice by taking goal priorities into account

By taking goal priorities into account when preparing financial advice for clients, advisors can suggest a minimum reservation on their client’s account. This can ensure there is a higher probability that high priority goals can be met later in time. In addition, advisors can provide insights on the expected budget that is available for low(er) priority goals. When monitoring these results over time, advisors can further improve the value and quality of advice towards their clients. By adopting an approach that fully puts client goals central in the advice process, the proposed strategy will also fully take the wishes and preferences of the client into account. A goal-based approach will provide a better conversation between advisor and client and can be communicated in a simple and more understandable way. This leads to a better and more suitable advice and as a result, increase client’s engagement and commitment to the plan.

For more information or details, do not hesitate to contact:

Ronald Janssen: +31652065657 | Ronald.Janssen@ortec-finance.comContact

Ronald Janssen

Head of Innovation & Research Global Wealth SolutionsRelated Insights

-

22 July 2026Article GLASS PRISM: The Evolution of Insurance Asset Portfolio Optimization

22 July 2026Article GLASS PRISM: The Evolution of Insurance Asset Portfolio OptimizationFollowing the launch of GLASS PRISM, Ortec Finance attracted significant media attention, with industry publications exploring how the solution is transforming portfolio optimization for institutional investors.

-

20 July 2026Articles GLASS PRISM: A New Standard in Strategic Asset Allocation

20 July 2026Articles GLASS PRISM: A New Standard in Strategic Asset AllocationThe GLASS PRISM launch introduces targeted SAA powered by scenario-based machine learning. Discover what's driving industry attention.

-

13 July 2026Will advisers have to reposition annual reviews as a premium service to justify their fees?

13 July 2026Will advisers have to reposition annual reviews as a premium service to justify their fees?Can advisers still justify ongoing fees without annual reviews? The FCA's shift may reshape advice business models.

-

09 July 2026Aviva partners with Ortec Finance to expand access to financial advice

09 July 2026Aviva partners with Ortec Finance to expand access to financial adviceAviva has selected Ortec Finance as its technology partner to enhance its customer guidance and financial planning proposition.

-

06 July 2026Quarterly Scenario Webinar Q3 2026 - Energy Shocks and Market Repricing: Navigating the Next Phase

06 July 2026Quarterly Scenario Webinar Q3 2026 - Energy Shocks and Market Repricing: Navigating the Next PhaseJoin our webinar to explore how renewed US–Iran military conflict could reshape energy markets, inflation, interest rates and investment portfolios.

-

18 June 2026Virtual panel discussion #2 (Asia-Pacific): Extending the lens on climate change to capital market assumptions

18 June 2026Virtual panel discussion #2 (Asia-Pacific): Extending the lens on climate change to capital market assumptionsHear thought-provoking perspectives on climate change’s impact on capital market assumptions, including short and longer-term market pricing dynamics

-

18 June 2026TPA Quick Wins Article

18 June 2026TPA Quick Wins ArticleHow to adopt the TPA framework without fully transitioning to TPA.

-

05 June 2026Strategic Asset Allocation in the “TW-ICS” Era

05 June 2026Strategic Asset Allocation in the “TW-ICS” EraHow Taiwanese insurers can modernize strategic asset allocation and strengthen long-term resilience.

-

05 June 2026Total Portfolio Lens Brochure

Total Portfolio Lens (TPL) is built for investors navigating whole-fund complexity: it connects forward-looking analytics to action and allows investors to evolve at a pace that fits their governance and readiness.